SPRINTERS VERSUS MARATHONERS

Leadership capabilities for a new era of private equity value creation

SPRINTERS

VERSUS MARATHONERS

Leadership capabilities

for a new era of private equity

value creation

Eighth Annual Private Equity (PE)

Leadership Survey

Turmoil and disruption in the business environment make leadership and talent strategy more important than ever for private equity firms and the companies they invest in. They will need new capabilities—and a stronger, more strategic approaches to leadership.

For eight consecutive years, AlixPartners has monitored the most-significant trends and developments affecting leadership in the private equity (PE) industry, through our annual survey of executives in PE firms and portfolio companies (portcos). This year our research is supplemented with insights from IPEM, a Paris-based association of European PE firms. To learn more, see the section “About Our Eighth Annual PE Leadership Survey” at the end of this report.

The 2023 PE Leadership Survey documents the importance of leadership as PE firms and portcos confront a difficult economic environment and a disrupted business climate; it also reveals how the challenges and opportunities businesses face put new and different demands on leaders in the industry. Leadership is essential as PE firms and portcos address a set of macroeconomic difficulties—a slowdown or recession, inflation, steeply rising interest rates, and geopolitical risks—alongside ongoing supply chain disruptions, accelerating technological change, a continuing war for talent, and a growing need to address environmental, social, and governance issues.

To meet those tests, both PE firms and portcos must look to their leadership for strategic ideas, smart initiatives, and strong execution. Leaders and leadership teams will need to be more capable. However, as the report shows, many players in the industry say that their leadership is not good enough or its ranks are too thin. Indeed, only a bare majority of respondents say their portfolio companies have the right leaders in place to deal with the multiple issues their enterprises face.

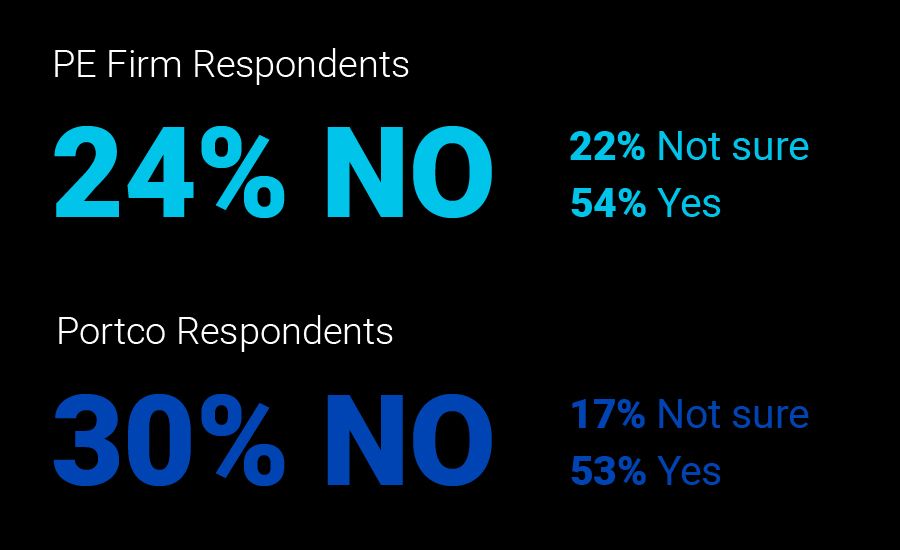

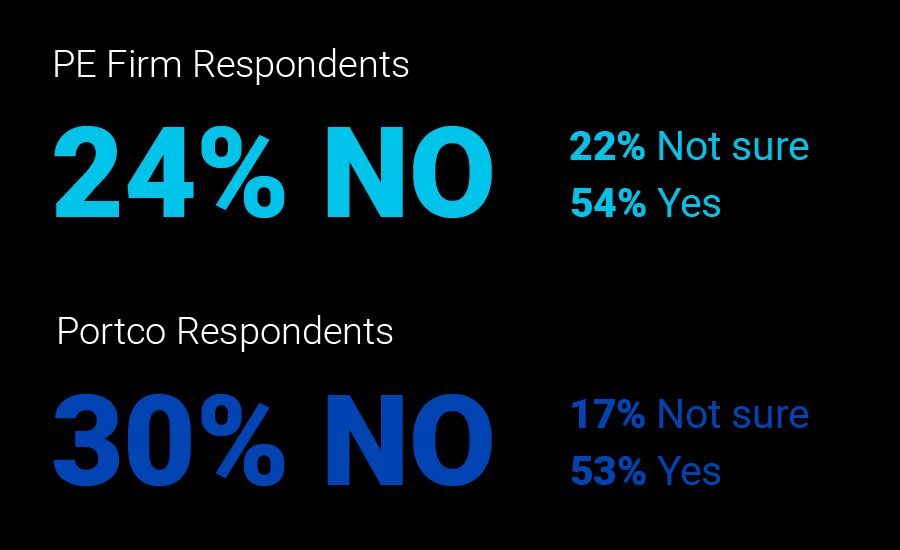

Do you have the right leaders in place?

This is a high-stakes business environment—one of those times when it really matters that you choose the right investments, lay out the right strategy, and get results fast.

Do you have the right leaders in place?

This is a high-stakes business environment—one of those times when it really matters that you choose the right investments, lay out the right strategy, and get results fast.

KEY FINDING #1:

A macroeconomic maelstrom has engulfed private equity

Global economic conditions in 2023 seem custom-designed to cause fits for PE. Slowing economic growth plus the danger—in some economies, the reality—of recession have flattened demand. The International Monetary Fund projects 2023 growth will be just 1.2% in advanced economies, less than half of what it was in 2022. Meanwhile, inflation, though slowing from its 2022 levels, remains stubbornly and dangerously high, especially outside the energy sector. That in turn has provoked central banks to raise interest rates, in turn raising the price of debt and reducing its availability. It is likely that the March collapse of Silicon Valley Bank will cause already jittery banks to be even more reluctant to lend except to the very highest-quality borrowers. Some public pension funds, which had been ardent investors in PE, are reducing their commitment to the industry.

About half of PE industry leaders expect, therefore, that deals will be fewer and take longer, and that exits will be harder and holding periods longer.

Among European industry leaders IPEM polled, 78% say 2023 is likely to be a bad year for exiting—though the same percentage says it will probably be a good year for deal making.

Inflation, interest rates, a slowdown, or a downturn—these, along with the continuing impact of the war in Ukraine and the persistent effects of COVID-19, mean that the economic and business environment weighs more heavily on the PE industry than it has in recent years. Two years ago, “market dynamics and disruption” ranked fourth in the priority list for PE and portco leadership, after strategy prioritization, communication, and execution. This year, three of the top five organizational challenges are economic.

Among European industry leaders IPEM polled, 78% say 2023 is likely to be a bad year for exiting—though the same percentage says it will probably be a good year for deal making.

Inflation, interest rates, a slowdown, or a downturn—these, along with the continuing impact of the war in Ukraine and the persistent effects of COVID-19, mean that the economic and business environment weighs more heavily on the PE industry than it has in recent years. Two years ago, “market dynamics and disruption” ranked fourth in the priority list for PE and portco leadership, after strategy prioritization, communication, and execution. This year, three of the top five organizational challenges are economic.

What this means: With deals delayed or more expensive, exits put on hold, and low economic growth, PE firms and the companies they own will be less able to create value through financial engineering. They cannot expect to be helped by the overall economy; instead, they are likely to be riding into economic headwinds or buffeted by the unexpected crosswinds of disruption. To deliver on their promises to investors and stakeholders, firms and companies in the PE industry will have to rely on their own energy, ingenuity, and execution. The PE industry will have to prioritize leadership and think hard about how leaders lead so that they create maximum value for their enterprises and enjoy the support of the rank and file.

KEY FINDING #2:

With portfolios under stress, the path to value creation has shifted

The economy will take a bite out of portco profitability as well as out of PE firm dealmaking. With debt more expensive and revenue growth slowed or nonexistent, portco executives will have to work harder for every dollar of EBITDA. For some, conditions will be rough indeed: Nearly half the PE leaders surveyed—47%—say they expect more portcos to become distressed, and another 17% have their fingers crossed, unsure of how their portcos will fare.

The path to value creation, therefore, goes directly through superior operating performance. Given the deal-making environment, holding times will be longer—meaning that value will be realized later and only after eight or more additional quarters of post-deal operations. In addition, fewer firms and portcos will pursue inorganic growth during the holding period. Among PE firm leaders, bolt-on acquisitions rank fifth among the value-creating levers, behind leadership, operating and organizational efficiency, and organic growth. Among portco leaders, acquisitions and divestitures don’t make the top-five list.

Instead, the task of value creation falls squarely on leading the business effectively and designing and operating it efficiently, with an eye toward revenue and margin growth and cost control. Some PE firms and portcos may face the difficult task of turning around a company that has become distressed by economic circumstances or rapidly changing industry dynamics.

The industry’s emphasis on organizational efficiency is noteworthy—that is, designing an enterprise that is inherently efficient, not just tightening up an existing organization. This implies business model change, through significant outsourcing, digital transformation, or other initiatives that fundamentally alter what work is done, how it is organized, and who does it. In the AlixPartners Disruption Index survey of 3,000 high-ranking executives worldwide, fully 98% say they expect their business model to change within three years. Among the fastest-growing companies in the survey, 57%—nearly three out of five—are changing their business models this year.

Organizational efficiency differs in kind from operational efficiency. PE industry veterans know the operational efficiency playbook by heart; it’s not easy, but it’s not unfamiliar. Business model transformation, on the other hand, calls for more imaginative strategic insights and higher-level leadership skills—for example, (1) using technology not just to automate processes but also to change how a company engages with customers, (2) inspiring colleagues not just to execute but also to innovate, and (3) not just rethinking what to do but also rethinking how to do it. It is a different leadership challenge—and it can sometimes seem to be at odds with operational efficiency. It is also anchored in behavior change, making it more difficult to attain and sustain—but more powerful once achieved.

The path to value creation, therefore, goes directly through superior operating performance. Given the deal-making environment, holding times will be longer—meaning that value will be realized later and only after eight or more additional quarters of post-deal operations. In addition, fewer firms and portcos will pursue inorganic growth during the holding period. Among PE firm leaders, bolt-on acquisitions rank fifth among the value-creating levers, behind leadership, operating and organizational efficiency, and organic growth. Among portco leaders, acquisitions and divestitures don’t make the top-five list.

Instead, the task of value creation falls squarely on leading the business effectively and designing and operating it efficiently, with an eye toward revenue and margin growth and cost control. Some PE firms and portcos may face the difficult task of turning around a company that has become distressed by economic circumstances or rapidly changing industry dynamics.

The industry’s emphasis on organizational efficiency is noteworthy—that is, designing an enterprise that is inherently efficient, not just tightening up an existing organization. This implies business model change, through significant outsourcing, digital transformation, or other initiatives that fundamentally alter what work is done, how it is organized, and who does it. In the AlixPartners Disruption Index survey of 3,000 high-ranking executives worldwide, fully 98% say they expect their business model to change within three years. Among the fastest-growing companies in the survey, 57%—nearly three out of five—are changing their business models this year.

Organizational efficiency differs in kind from operational efficiency. PE industry veterans know the operational efficiency playbook by heart; it’s not easy, but it’s not unfamiliar. Business model transformation, on the other hand, calls for more imaginative strategic insights and higher-level leadership skills—for example, (1) using technology not just to automate processes but also to change how a company engages with customers, (2) inspiring colleagues not just to execute but also to innovate, and (3) not just rethinking what to do but also rethinking how to do it. It is a different leadership challenge—and it can sometimes seem to be at odds with operational efficiency. It is also anchored in behavior change, making it more difficult to attain and sustain—but more powerful once achieved.

What this means: For some time, the PE industry has faced diminishing returns from financial engineering, as a growing amount of capital chases an unchanging number of potential deals, thus competing away the advantage that capital can create by itself. The tough economics of 2023 make it even clearer: The road to value runs through operating partners and portco executives.

Leadership is the key: the ability to set goals and a vision, establish priorities, and motivate and organize people. The next two sections of this report describe some of those challenges in more detail. As we will see, there are significant differences in emphasis between PE firms and their portco managers about what leadership capabilities are necessary to achieve these goals—but both of them clearly see that strong leadership and efficient execution define the path to success.

KEY FINDING #3:

Intensifying operational challenges demand vigorous attention

A down market puts pressure on operations, as companies try to keep costs commensurate with revenues. Nearly four out of ten companies told AlixPartners last fall that they had already prepared action plans for a downturn, with expense reduction at the top of the list of actions they had taken.

Efficiency is not enough, however, as the PE Leadership Study data show. Unless cost-cutting is accompanied by rethinking how work gets done, organizations get thinned out and brittle; they lose both resilience and the ability to respond quickly to disruption.

The need to avoid sacrificing resilience on the altar of cost is particularly clear in supply chain operations. Though stories about supply chain disruption have moved off the front pages of newspapers, 52% of executives say supply chain disruption is more of a challenge for their company than it was a year ago. PE firms feel the impact most in their ability (or inability) to pass on costs with higher prices; 51% of PE executives cite that issue, vs. 34% of portco leaders. Portcos are more acutely affected by the impact of supply chain disruption on forecasting: 42% say supply chain disruptions have led to difficulty in forecasting revenues and profits, compared to just 34% of PE leaders.

Because the problem is both severe and enduring, the solutions must be both long- and short-term. The data show it:

- Nine out of 10 CEOs told the AlixPartners Disruption Index that their companies need to take such measures as diversifying their supply base, investing in AI solutions to combat disruption, and entirely rethinking supply chain management.

- At the same time, 90% of both PE and portco executives told us they expect to see results from their supply chain actions within a year.

Though they recognize the need for long-term fixes, only about a third of companies have actually made them. In the PE industry, the financial focus of PE firms might be one reason there is more talk than action when it comes to structural change. PE firms are eight percentage points more likely than portcos to want to respond to supply chain problems with price increases. Price increases are the first-choice tools of portco executives, too, but those executives place more overall emphasis on long-term changes (such as diversifying the supply base, transforming procurement, and increasing efficiency) than their PE investors do.

Because the problem is both severe and enduring, the solutions must be both long- and short-term. The data show it:

- Nine out of 10 CEOs told the AlixPartners Disruption Index that their companies need to take such measures as diversifying their supply base, investing in AI solutions to combat disruption, and entirely rethinking supply chain management.

- At the same time, 90% of both PE and portco executives told us they expect to see results from their supply chain actions within a year.

Though they recognize the need for long-term fixes, only about a third of companies have actually made them. In the PE industry, the financial focus of PE firms might be one reason there is more talk than action when it comes to structural change. PE firms are eight percentage points more likely than portcos to want to respond to supply chain problems with price increases. Price increases are the first-choice tools of portco executives, too, but those executives place more overall emphasis on long-term changes (such as diversifying the supply base, transforming procurement, and increasing efficiency) than their PE investors do.

What this means: There’s tension between short- and long-term responses to supply chain disruption and other operating issues: on one hand are the just-raise-prices quick fix and the desire to see results within a year; on the other is the intention to make deep changes in structure, supplier networks, and capabilities.. The job of leadership is to resolve these tensions—not by picking one over the other, but by finding and demanding solutions that achieve both. For example, it is possible to build supply chain control towers powered by AI and to do it within months. As hold times lengthen, it will become more important for PE-owned enterprises to do the structural work. Another promising avenue: make progress in two directions by adding not just more suppliers, but also more woman- and minority-owned suppliers that could also support long-term efforts to reduce dependence on overseas suppliers.

KEY FINDING #4:

Organizational models are changing as technology accelerates

There is a clear change in the technology agenda for PE-owned businesses. While table-stakes technology capabilities like cybersecurity, automation, and cloud migration remain critical, companies are shifting a greater percentage of their investment into technologies that provide real-time data and analysis for decision support. Interestingly, PE firms emphasize technology more than portcos do almost across the board—the reverse of what we see with operations and supply chain issues.

PE leaders see three kinds of benefits from their portcos’ use of technology. About three out of five (61%) envision big opportunities from turning data into insights—seeing the business better. Half (52%) want portcos to use technology to push productivity up and costs down—running a tighter ship. Third, there is a strongly emerging emphasis on revenue-enhancing opportunities from technology—driving organic growth. Substantial numbers of PE leaders are urging their portcos to employ technology that helps them acquire more customers (35%), to devise new, higher-revenue business models (34%), and to increase customer intimacy (30%). It’s a shift from digital on the inside (operations and control) to digital on the outside (customer experience and revenue).

Except for data visualization, the portcos seem less convinced—or perhaps less certain—about how to establish priorities. In the AlixPartners Disruption Index survey, 94% of the fastest-growing companies say they have enough resources for their technology investments—but even so, 65% say they felt change was happening so fast they couldn’t keep up. In this environment, PE-owned companies might have an advantage from ownership support. Among CEOs overall, 83% say that their board of directors impedes the process of adopting new technology. But the PE Leadership survey data show the reverse: PE leadership—the owners—are highly supportive of digital investment. Perhaps what’s missing are concrete plans to turn that enthusiasm into profitable projects.

What this means: PE-owned businesses—like all others—are making the shift from digitization (using digital to increase efficiency, cut costs, and automate) to digital transformation (using digital to fundamentally change how work is done, how customers are served, and how value is created). This shift puts new responsibilities and pressures on leaders, who must themselves become more digitally savvy than their predecessors. More than that, they need to be digital in a practical way: that is, to understand where and how digital can be part of the solution to the business problems they face, rather than to pursue tech for tech’s sake. By prioritizing business goals first, leaders can then prioritize technology moves. PE firms, for their part, can play a valuable role in sharing insight, knowledge, and perhaps technology across their portfolios.

KEY FINDING #5:

Amid the storm, PE firms and portcos face a leadership gap

Everything in the business environment—a tough economy, longer hold periods, a stonier path to EBITDA growth, operational and technological disruptions—points to the need for leadership: leadership that can define what needs to be done; leadership that gets things done. For PE firms, leadership effectiveness is the #1 lever for value creation, cited by 70% of survey respondents.

Yet, as we noted earlier, barely half of PE firms and portcos say they have the leaders they need. Asked if the companies they oversee have the right leaders in place, 30% of portco executives bluntly say no while 17% are unsure. Just 53% can answer, yes.

The problem isn’t just recruiting. Most PE firms and portcos say they are competing fairly well in the war for talent, with more than two-thirds saying they have been able to hire at expected rates or better. That doesn’t mean recruiting is easy—and the talent issue isn’t only about finding people. Recruiting and retaining talent is the #1 challenge portco executives face, named by 81%—far more than any other issue. Among PE executives, the war for top talent is one leg of a three-legged stool of human capital concerns—cited by 41%, alongside burnout (42%) and retention (41%). European PE executives say virtually the same: the war for talent is cited by 42% and burnout by 45%, while retention is of slightly less concern at 36%.

Furthermore, the talent gap isn’t just at the top; skills, particularly technical skills, have an important place on the industry’s talent agenda—especially for portcos, as one would expect. In the AlixPartners Disruption Index survey, three out of five executives say that the pace of change is making skills rapidly obsolete, and while only 27% say hiring overall has become harder, 40% say finding the right skills is difficult. In addition, 63% said that shifts in workforce values and preferences—meaning, generational divides—are driving disruption in their companies.

PE firms and portcos see diversity—in expanding the talent pool—as one way to close their human capital gap. PE firms put a growing emphasis on ESG—environmental, social, and governance issues, which include diversity. Sixty-nine percent see ESG as a lever for value creation (up from 53% last year). The same percentage of PE leaders are willing to invest in ESG whether or not they see an immediate return; indeed, three times more PE firms increased ESG spending last year than decreased it. Portcos seem less convinced. Twenty-one percent have increased spending on ESG—but 19% have cut it. Just 40% say they would invest in it regardless of returns.

What this means: The executive and employee value proposition needs to change to reflect the combination of longer hold times and the need to build and innovate as well as operate and cut costs. The days of the old-school PE model—buy a company, load it up with debt and its executives with incentives, and work like hell for five years—are over.

PE will never be an industry that tolerates gentleman’s C performance, but the industry needs to offer reasons to come and reasons to stay that amount to more than the promise of a big payoff in five years. That means bringing culture, engagement, career pathing, and other issues into the management repertoire of portcos—and ensuring that PE firms understand the importance of these initiatives.

Everything in the business environment—a tough economy, longer hold periods, a stonier path to EBITDA growth, operational and technological disruptions—points to the need for leadership: leadership that can define what needs to be done; leadership that gets things done. For PE firms, leadership effectiveness is the #1 lever for value creation, cited by 70% of survey respondents.

Yet, as we noted earlier, barely half of PE firms and portcos say they have the leaders they need. Asked if the companies they oversee have the right leaders in place, 30% of portco executives bluntly say no while 17% are unsure. Just 53% can answer, yes.

The problem isn’t just recruiting. Most PE firms and portcos say they are competing fairly well in the war for talent, with more than two-thirds saying they have been able to hire at expected rates or better. That doesn’t mean recruiting is easy—and the talent issue isn’t only about finding people. Recruiting and retaining talent is the #1 challenge portco executives face, named by 81%—far more than any other issue. Among PE executives, the war for top talent is one leg of a three-legged stool of human capital concerns—cited by 41%, alongside burnout (42%) and retention (41%). European PE executives say virtually the same: the war for talent is cited by 42% and burnout by 45%, while retention is of slightly less concern at 36%.

Furthermore, the talent gap isn’t just at the top; skills, particularly technical skills, have an important place on the industry’s talent agenda—especially for portcos, as one would expect. In the AlixPartners Disruption Index survey, three out of five executives say that the pace of change is making skills rapidly obsolete, and while only 27% say hiring overall has become harder, 40% say finding the right skills is difficult. In addition, 63% said that shifts in workforce values and preferences—meaning, generational divides—are driving disruption in their companies.

PE firms and portcos see diversity—in expanding the talent pool—as one way to close their human capital gap. PE firms put a growing emphasis on ESG—environmental, social, and governance issues, which include diversity. Sixty-nine percent see ESG as a lever for value creation (up from 53% last year). The same percentage of PE leaders are willing to invest in ESG whether or not they see an immediate return; indeed, three times more PE firms increased ESG spending last year than decreased it. Portcos seem less convinced. Twenty-one percent have increased spending on ESG—but 19% have cut it. Just 40% say they would invest in it regardless of returns.

What this means: The executive and employee value proposition needs to change to reflect the combination of longer hold times and the need to build and innovate as well as operate and cut costs. The days of the old-school PE model—buy a company, load it up with debt and its executives with incentives, and work like hell for five years—are over.

PE will never be an industry that tolerates gentleman’s C performance, but the industry needs to offer reasons to come and reasons to stay that amount to more than the promise of a big payoff in five years. That means bringing culture, engagement, career pathing, and other issues into the management repertoire of portcos—and ensuring that PE firms understand the importance of these initiatives.

KEY FINDING #6:

PE firms see leaders as change agents

PE executives are keenly focused on the team at the top, the portco leaders with whom they interact frequently. Asked about the most important talent issues to focus on, they are twice as likely to cite the quality of the executive team as portco leaders are. (Those portco leaders are the team in question, of course.) For their part, portco leadership is far more concerned with overall talent strategy than PE investors are—71% more concerned.

Underlying this difference are profoundly divergent views of what leaders ought to be doing. Both PE firm and portco executives recognize the critical role of leadership in setting enterprise strategy. But when it comes to turning strategy into reality—from vision to plan, from forecast to results, and from deal thesis to value creation—there’s a difference.

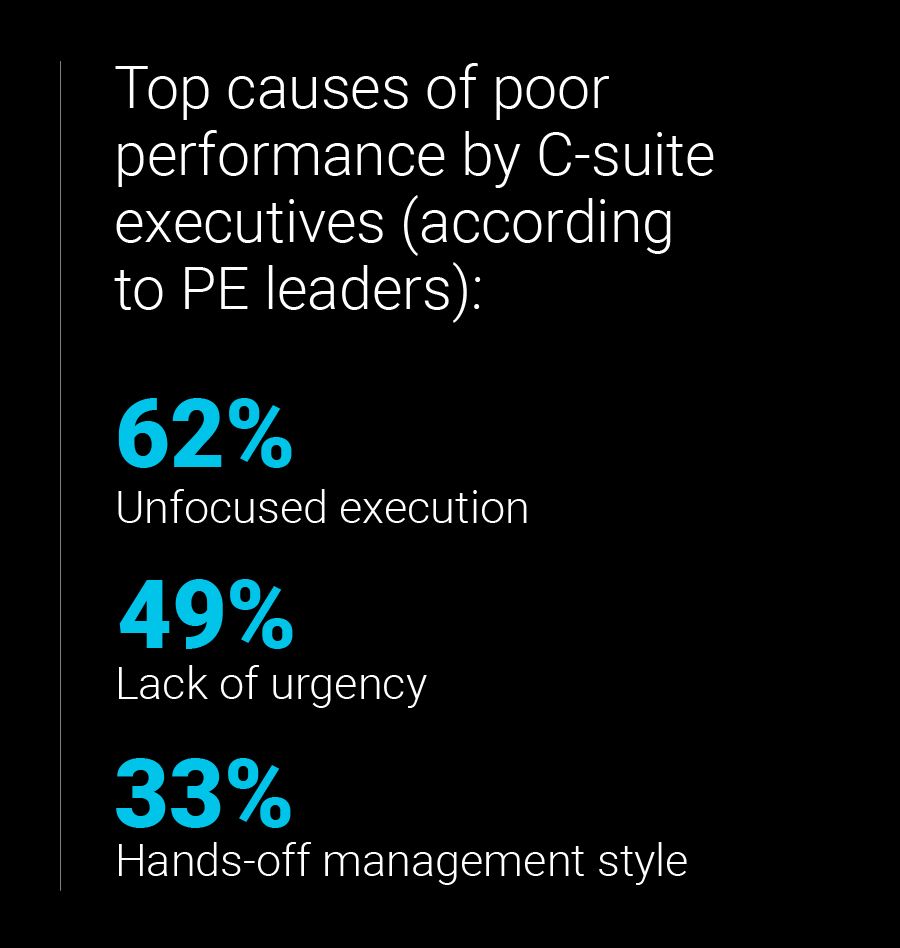

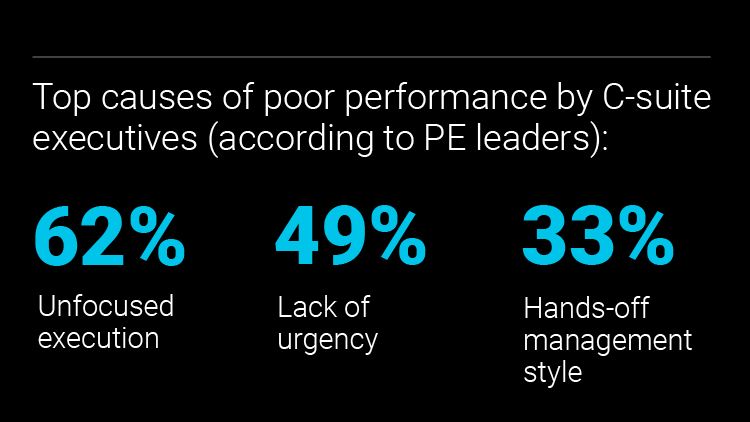

In the PE mind, leadership is heroic. The best leaders drive change, motivate their troops, are resilient and agile; they see the big picture. To PE leaders, these traits matter because they have the greatest impact on generating high returns for investors. When things go wrong, in their view, it’s because leadership has been unfocused in execution, not urgent enough in how it executes, or too hands-off.

Lack of capability in execution is also the biggest cause of failure specifically for CEOs, again in the view of PE firms. A lack of people skills comes a distant second, cited by only two-thirds as often as weakness in execution.

PE wants hard-driving leaders. It wants stars. Given that focus on individual leaders, it is no wonder that PE executives worry about their burning out or leaving or being hard to replace.

In the PE mind, leadership is heroic. The best leaders drive change, motivate their troops, are resilient and agile; they see the big picture. To PE leaders, these traits matter because they have the greatest impact on generating high returns for investors. When things go wrong, in their view, it’s because leadership has been unfocused in execution, not urgent enough in how it executes, or too hands-off.

Lack of capability in execution is also the biggest cause of failure specifically for CEOs, again in the view of PE firms. A lack of people skills comes a distant second, cited by only two-thirds as often as weakness in execution.

PE wants hard-driving leaders. It wants stars. Given that focus on individual leaders, it is no wonder that PE executives worry about their burning out or leaving or being hard to replace.

What this means: Operating partners rightly zero in on the first year of ownership—the critical first few quarters during which they and their portco counterparts need to capture synergies and get a running start on value creation. Hence, too, their emphasis on focus and urgency. It’s very important that portco executives understand and share views about those priorities so that communication between ownership and management can be open and clear; success in those early quarters builds both trust and capabilities for the out years, when the leadership agenda changes.

KEY FINDING #7:

Portcos emphasize the role of leaders as team builders

The leader portco executives see is a team player and team builder. Yes, this leader is also a motivator who pushes for change, but the changes happen because of the implementation of collaborations, because of the building of relationships, and because the leader has assembled a bench of talented people.

Indeed, PE and portco company leaders have strikingly different views of how human capital creates value:

- Leadership effectiveness gets more weight from PE leaders, 70% of whom cite it as a top priority for creating value (indeed, it is their #1 priority); 58% of portco leaders say the same. As a lever for value creation, leadership effectiveness ranks second among portcos, after organic growth.

- Talent strategy (recruiting, retaining, etc.)—matters virtually equally to both—31% for PE, 33% among portcos.

- Culture is seen and prioritized as a lever for value almost three times more often by portco leaders (33%) than by PE leaders (12%).

Portco leaders see talent strategy as a multifaceted thing. Leadership competencies such as succession planning and relationship building are two and a half times more important to portco executives than to PE executives.

Why the differences? Perhaps it’s because PE operating partners prefer to delegate this part of the agenda to the people in direct charge of the portfolio companies. More likely, each group sees value creation through the lens of its own experience: dealmakers see value coming from a small team with a brilliant idea; operators see it coming by organizing, aligning, and motivating a large group toward a shared goal.

Whatever the cause, the difference in mindset can produce misalignment between operating partners and portfolio leadership. In general, portcos have fewer complaints about their investors than vice versa. PE firms’ top grievances with management were cited by 62% (unfocused execution) and 49% (lack of urgency); while the top-ranking complaints by portcos about operating partners were named by just 28% (lack of business acumen, too hands-on).

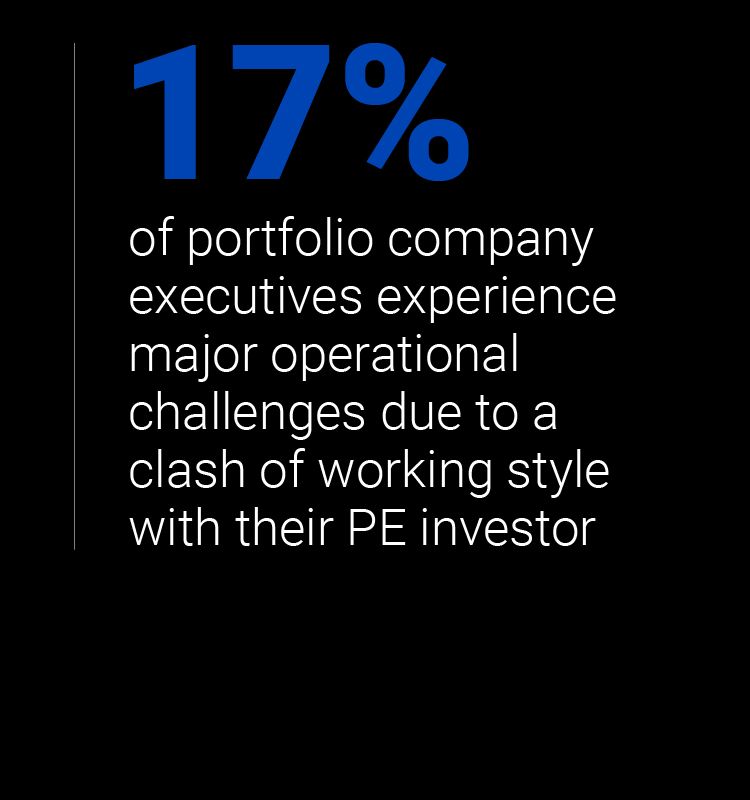

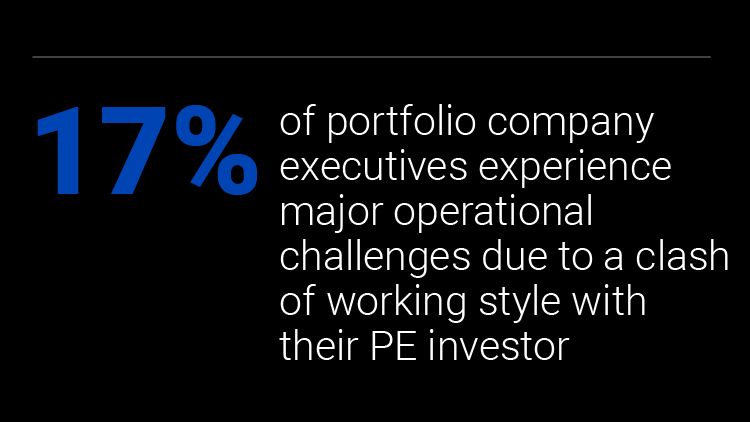

Competing points of view can produce constructive tension. But nearly one out of five portco executives say that a clash of working styles with their PE investor is a major operational challenge.

The leader portco executives see is a team player and team builder. Yes, this leader is also a motivator who pushes for change, but the changes happen because of the implementation of collaborations, because of the building of relationships, and because the leader has assembled a bench of talented people.

Indeed, PE and portco company leaders have strikingly different views of how human capital creates value:

- Leadership effectiveness gets more weight from PE leaders, 70% of whom cite it as a top priority for creating value (indeed, it is their #1 priority); 58% of portco leaders say the same. As a lever for value creation, leadership effectiveness ranks second among portcos, after organic growth.

- Talent strategy (recruiting, retaining, etc.)—matters virtually equally to both—31% for PE, 33% among portcos.

- Culture is seen and prioritized as a lever for value almost three times more often by portco leaders (33%) than by PE leaders (12%).

Portco leaders see talent strategy as a multifaceted thing. Leadership competencies such as succession planning and relationship building are two and a half times more important to portco executives than to PE executives.

Why the differences? Perhaps it’s because PE operating partners prefer to delegate this part of the agenda to the people in direct charge of the portfolio companies. More likely, each group sees value creation through the lens of its own experience: dealmakers see value coming from a small team with a brilliant idea; operators see it coming by organizing, aligning, and motivating a large group toward a shared goal.

Whatever the cause, the difference in mindset can produce misalignment between operating partners and portfolio leadership. In general, portcos have fewer complaints about their investors than vice versa. PE firms’ top grievances with management were cited by 62% (unfocused execution) and 49% (lack of urgency); while the top-ranking complaints by portcos about operating partners were named by just 28% (lack of business acumen, too hands-on).

Competing points of view can produce constructive tension. But nearly one out of five portco executives say that a clash of working styles with their PE investor is a major operational challenge.

What this means: Portco leaders want their operating partners to spend more time with them in developing strategic perspectives and building relationships—and they need more understanding and support from investors about the long-term leadership capabilities the company will need to thrive. Portcos place less value on operating partners’ efforts to lead change than the partners themselves do.

An agenda for action:

next steps for PE firms and portcos

Three years ago, the economy was sailing ahead in what turned out to be the last days of a sustained, gentle tailwind. Then came COVID, with its whipsaw of bust and boom. Now we have entered a period when interest rates are high (and staying high) and growth is low (and staying low for several quarters at least). Many deals made not long ago were predicated on an economy that is gone and deals yet to be made will need to account for circumstances not familiar even to ten-year veterans of the PE industry.

The disruption of the industry has major implications for leadership and leadership strategy. Here are four actions that PE firms and portcos should take both individually and together.

1. MAKE A REVIEW OF YOUR DEAL THESIS WITH A LEADERSHIP LENS

Longer hold times, a cooler economy, and a balance sheet with more equity and higher-priced debt should cause you to rerun the numbers to identify where the growth you need will come from. That, in turn, should lead you to assess your leadership team against the capabilities you now need, versus the skills that were the right ones before.

In the short run, you probably need a team that can jumpstart value creation with bold post-deal integration and transformation. Looking to the out years, however, the sources of value may change. You may need a digital transformation of the customer experience. You might need modernization of internal processes. And you might need to bank more on organic growth than on bolt-ons.

As you reaffirm or revise your deal thesis, consider the leadership capabilities needed to execute each element of the thesis. Will you need to add muscle to functions that are now skeletal? Will you need to build an innovation capability?

2. ASSESS YOUR LEADERSHIP TEAM AGAINST YOUR STRATEGIC NEEDS

How well matched is your current leadership team to the deal thesis and strategic vision you have just laid out? Given longer hold times, you may learn that you need fewer sprinters and more stretch runners on your team. Do you have the right mix of hard-nosed cost cutters and far-sighted innovators? Should your chief information officer be an efficiency type or a digital transformation type? If organic growth will be a greater part of your value-creating thesis, what kinds of leadership capabilities will you need? Think, for example, about your sources of revenue: Will you be pursuing more of a share-of-wallet strategy, emphasizing customer retention and loyalty, or a share-of-market strategy, emphasizing finding new customers or opening new markets? Given that strategy, do you have the right mix of farmer types and hunter types among your sales and marketing leaders?

In our experience, this kind of executive assessment is most effective when it (1) it is conducted across the leadership team, (2) it takes account of strategy and the paths to value creation, and (3) it is undertaken as a collaboration between PE firm and portco, which both cements the connection of leadership capability to deal thesis and increases buy-in by both parties in developing a long-term portco talent strategy.

3. BUILD UP YOUR TALENT MACHINE

Data from this year’s PE Leadership Survey underscore what we have seen in many years of working in this area: As a whole, the industry and its portfolio companies underinvest in building the capabilities on which long-term talent strategy depends. For example, PE firms and portcos are better at knowing who their key players are than they are at identifying or preparing successors, for example. In part, that represents a difference in perspective between PE firm and portco. In terms of delivering results in the current environment, PE firms place about twice as much emphasis on the quality of the executive team as portcos do; for their part, portcos think talent strategy is about twice as important as PE firms think it is. Across the industry generally, succession planning, bench-building, learning and development, and diversity, equity, and inclusion—all of them long-term talent investments—get less emphasis than they should, given the changing economies of the industry.

A critical first step involves Identifying key roles across the portco, ensuring they are staffed by A players, and developing succession plans for every such role.

4. TAKE A BEST-OF-BOTH-WORLDS APPROACH TO DIFFERENT LEADERSHIP STYLES

The most successful leaders are not just change agents or team builders—they are both. Transformational leadership combines strategic vision, the power to motivate, and a clear-eyed focus on execution via soft-side leadership competencies such as communication, relationship development, empathy, and compassion. Transformational leadership is no longer a nice-to-have in the PE industry. The fundamental, long-term trends and changes in the economics of the industry mean that the industry's continued success depends on a highly complementary combination of brilliant deal-making, rigorous execution, and long-term capability building. Competency in transformative leadership will greatly assist in the resolution of emerging complexities by building new relationships, fixing burnout through compassion and empathy, and instilling resilience through inspiration.

Divergent views of what leadership is can—and should—and must—converge around an agreed-upon, underwriteable strategy for value creation. On that basis, PE firms and portcos should be able to find ways to leverage each other’s strengths. Strong alignment between ownership and management is a proven path to profit.

Connect with the authors

ABOUT OUR EIGHTH ANNUAL PE LEADERSHIP SURVEY

Each year, findings from the AlixPartners PE Leadership Survey deliver valuable insights on themes relevant to the success of private equity (PE) investments. In previous years, themes we explored included:

- Key success factors in the first 100 days after a PE investment deal

- The impact of portcos’ human capital management practices on PEs’ internal rates of return

- New imperatives that portco and PE leaders must meet during times of disruption

- The role of a portco’s organizational culture in investment performance

This year’s survey was administered online from October through December 2022. Respondents consisted of 145 PE firm managing directors, operating partners, or founders, and 53 portfolio company (portco) directors, the majority of whom are CEOs or CFOs. Seventy-five percent of the PE firm respondents are with companies based in North America, as are 79% of the portco respondents. The largest share of portco respondents (42%) were with companies registering annual revenues of $100 million to $500 million, with another 30% coming from companies with annual revenues of less than $100 million. Thirty-eight percent of PE firm respondents reported their firms’ assets under management as less than $5 billion; another 30% have assets under management (AUM) between $5 billion and $20 billion.

We collaborated with IPEM, a Paris-based association for European PE investments, in its survey of 188 European PE investors and managers, and we include some of their perspectives in this report.

VIEW RESULTS FROM PREVIOUS YEARS' SURVEYS