2024 MEDIA & ENTERTAINMENT INDUSTRY PREDICTIONS REPORT

The media and entertainment industry has always been a poster child of creative destruction. But in recent decades, digital disruption has tested tried-and-true business models as new technologies, new entrants, and shifting consumer behaviors accelerate waves of innovation and change.

The result is a proliferation of content fragmented across multiple platforms, digital networks, and channels. All are competing for a share of consumer discretionary spend and advertising dollars—both of which have been adversely affected by strong macro headwinds as well as consumer fatigue and frustration.

Legacy media businesses such as broadcasters, publishers, and traditional advertising channels—which historically were able to extract a significant share of value from media profit chains—must adapt to this evolving ecosystem to survive. Meanwhile, emerging players must vigilantly defend their competitive moat in an increasingly crowded environment. Taking their eye off the ball for even a moment could allow others to jump ahead.

APPETITE FOR DISRUPTION:

WHAT'S NEXT IN MEDIA AND THE ENTERTAINMENT INDUSTRY FOR 2024

1. Wholesale distribution will fuel subscriber growth for streaming services.

This will bring operators and streamers together as companies search for a long-term replacement for the Pay TV model.

2. Artificial intelligence will transform the operational and competitive landscape...

...but successful integration hinges on a deliberate approach, data transformation, and change management—although we do not expect generative AI to replace human creative output, especially around premium content.

3. Moderate ad market recovery and mid-single-digit growth is likely...

...but this hinges on macroeconomic conditions that remain unclear.

4. Regulatory scrutiny and a high cost of capital will limit a rebound in M&A activity...

...but legacy media carve-out activity will drive dealmaking.

5. 2024 will be a year of reinvention and reinvestment in local news.

In which the traditional business model can evolve with new ideas and approaches.

01/05

Wholesale distribution will fuel subscriber growth for streaming services.

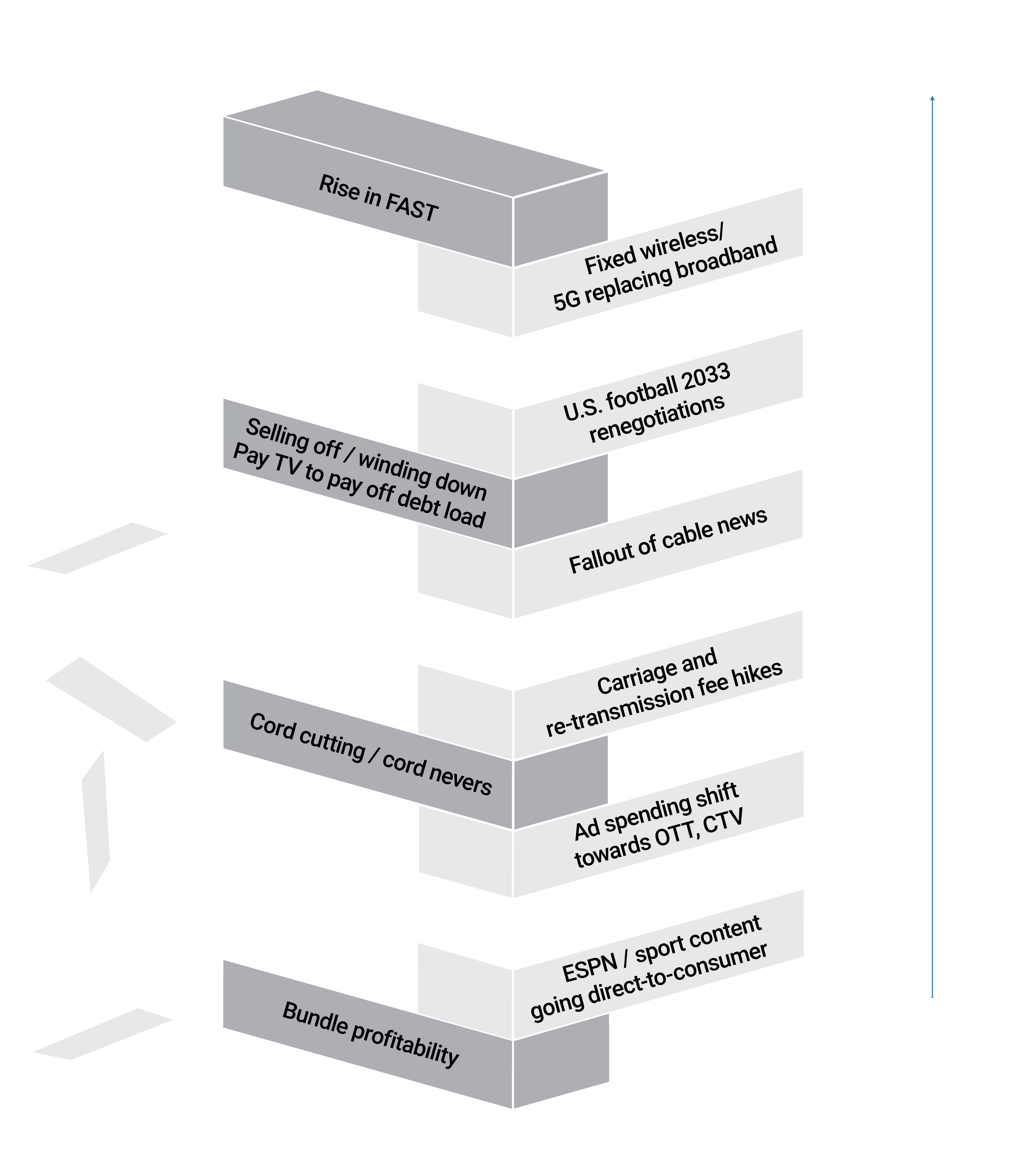

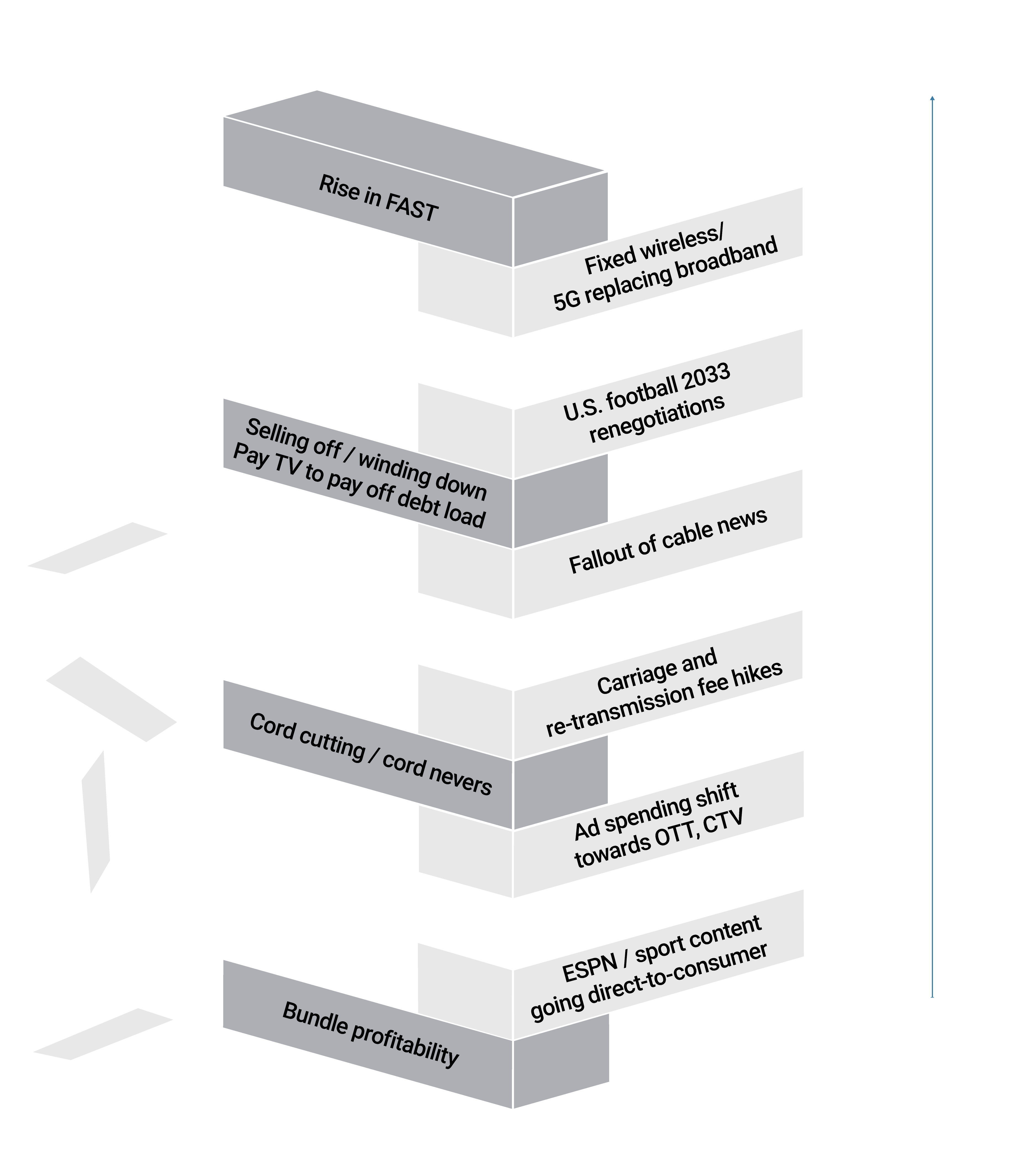

Even with the growth of streaming, a future model to replace the highly profitable Pay TV structure has yet to take shape in a way that satisfies both industry players and consumers.

While the future model remains uncertain, wholesale distribution deals are bringing operators and streaming services together—a strategy that diverges from the “emulate Netflix” trend of the late 2010s.

In July, we wrote about how the decline of the Pay TV bundle operates like a game of Jenga. Each new disruption is like pulling another block out of the tower. Unless Pay TV operators pivot, it’s only a matter of time before the whole tower topples over.

In August, the tower started to shake with the Charter-Disney carriage dispute. Stock prices in the ecosystem plunged as TV industry players and investors waited to see if the tower would topple. The negotiated agreement served as a block pulled out without collapsing the tower.

In the wake of the Charter and Disney agreement, it's evident that traditional Pay TV providers are not ready to go down without a fight. Cable providers know higher carriage fees will not continue to offset lost revenues from a declining subscriber base, especially as programmers move more premium content exclusively to direct-to-consumer (DTC).

In Charter's case, its weakness acted as a strength. Through preemptive diversification away from Pay TV as a main source of revenue, the company claims to have “reached the point of economic indifference” with its Pay TV business model. Calling attention to DTC vulnerabilities demonstrated that programmers have more to lose in this evolving landscape, and the proof is in the bottom line. Disney could have lost $4 billion in yearly free cash flow (FCF) without the new agreement, according to Oppenheimer estimates.

Global TV market growth will begin to level off as Pay TV revenues continue to shrink and the streaming market continues to mature.

As a result of a tapering CAGR, it is unlikely the market will support the 80+ streaming players that exist today globally, leading to streaming consolidation in 2024. In the U.S., we foresee streaming as a “winner-take-most” market with 4-5 winners.

Figure 1: What has propped up the Pay TV bundle? And what will fall?

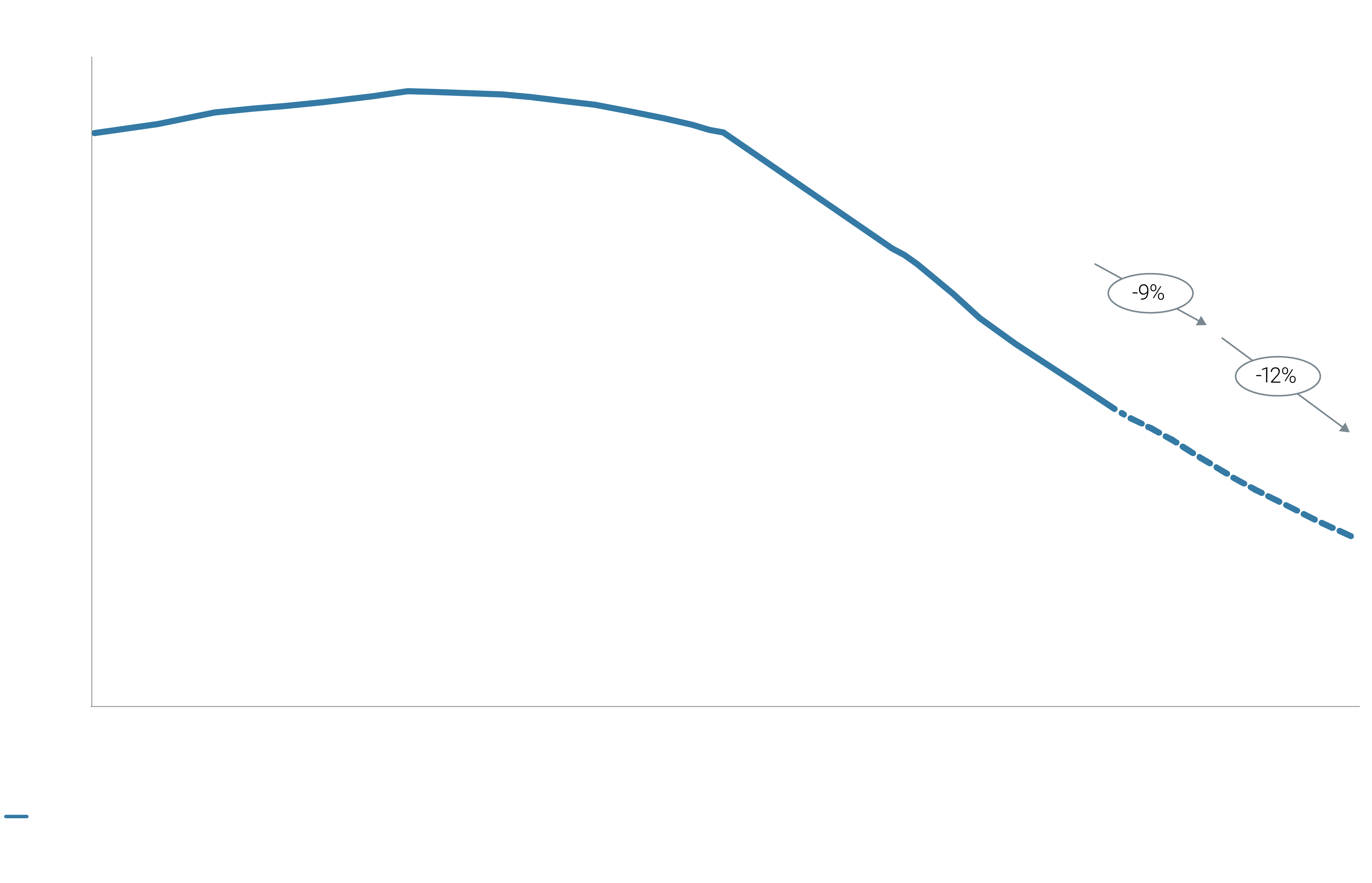

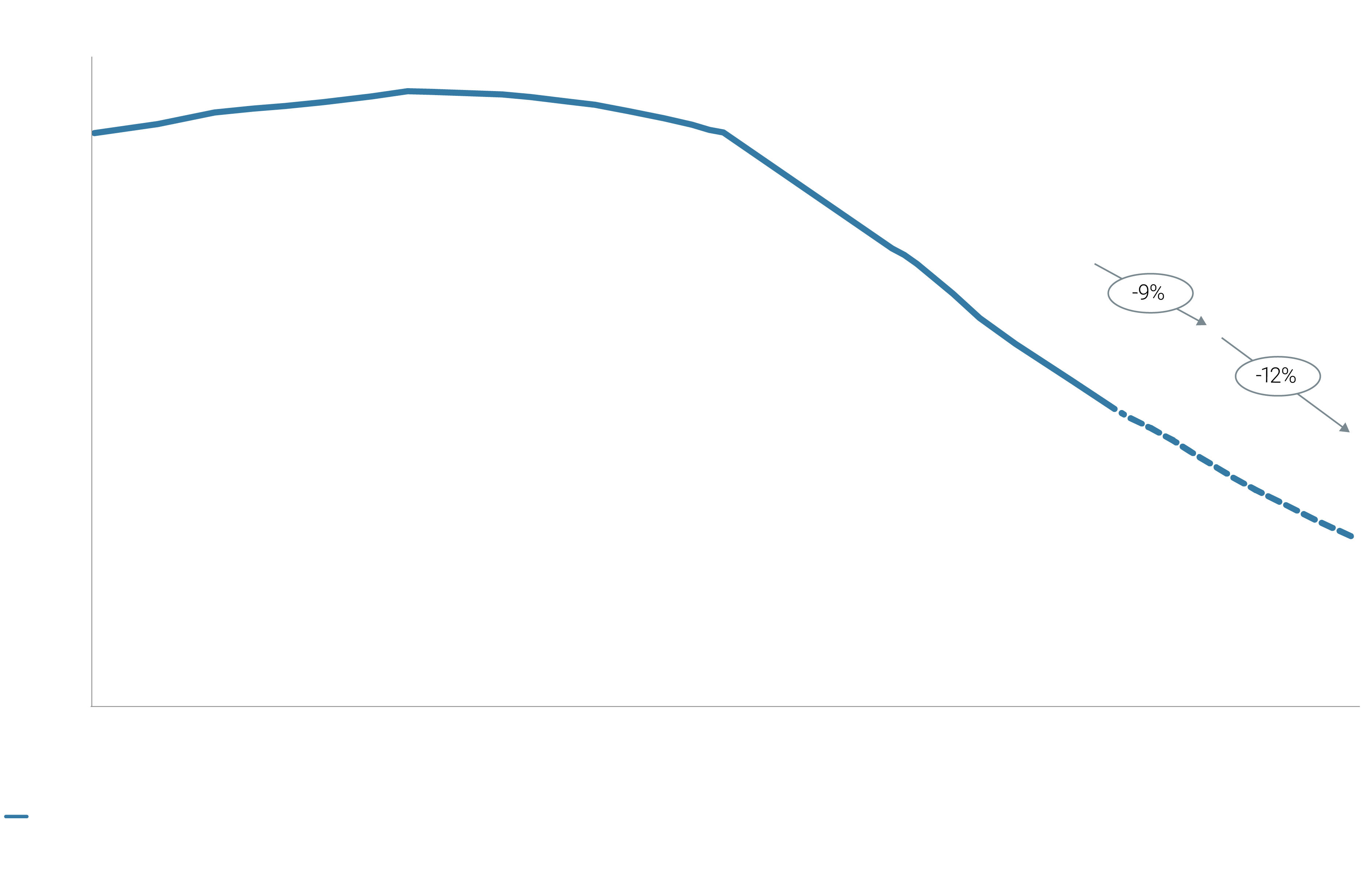

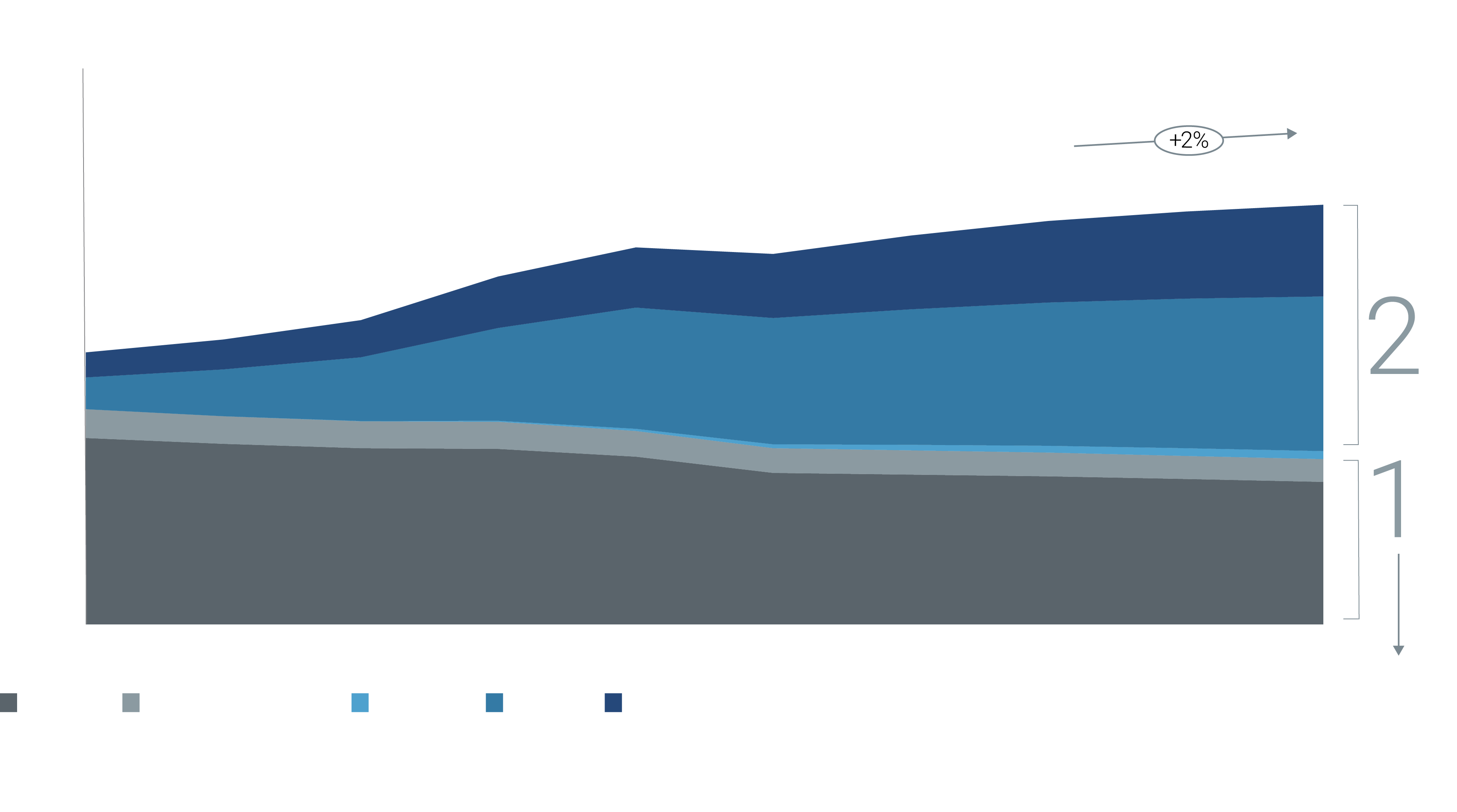

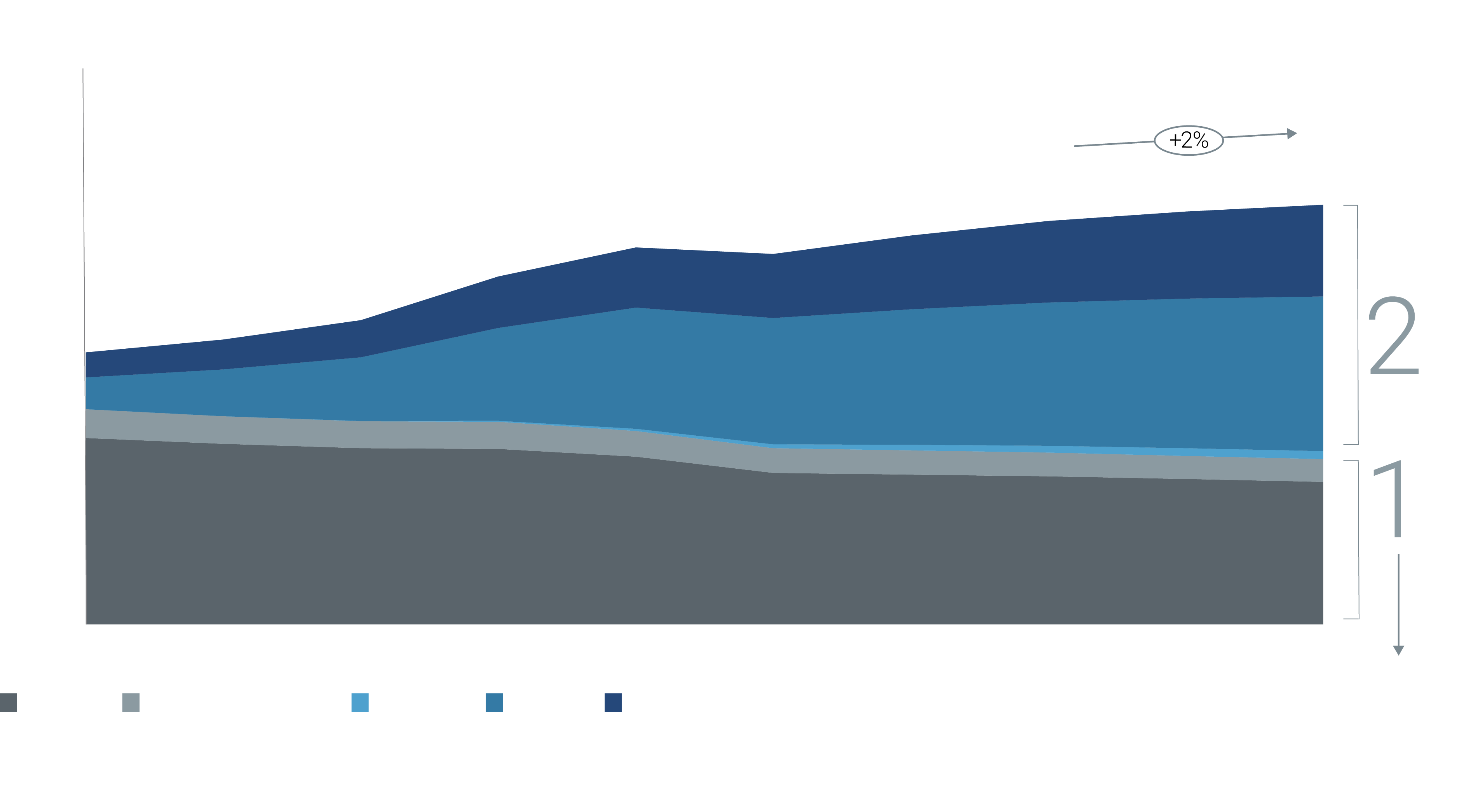

Figure 2: AlixPartners Proprietary Cord-Cutting Model, U.S. Households (MM)

Even with the growth of streaming, a future model to replace the highly profitable Pay TV structure has yet to take shape in a way that satisfies both industry players and consumers.

While the future model remains uncertain, wholesale distribution deals are bringing operators and streaming services together—a strategy that diverges from the “emulate Netflix” trend of the late 2010s.

In July, we wrote about how the decline of the Pay TV bundle operates like a game of Jenga. Each new disruption is like pulling another block out of the tower. Unless Pay TV operators pivot, it’s only a matter of time before the whole tower topples over.

In August, the tower started to shake with the Charter-Disney carriage dispute. Stock prices in the ecosystem plunged as TV industry players and investors waited to see if the tower would topple. The negotiated agreement served as a block pulled out without collapsing the tower.

Figure 1: What has propped up the Pay TV bundle? And what will fall?

In the wake of the Charter and Disney agreement, it's evident that traditional Pay TV providers are not ready to go down without a fight. Cable providers know higher carriage fees will not continue to offset lost revenues from a declining subscriber base, especially as programmers move more premium content exclusively to direct-to-consumer (DTC).

In Charter's case, its weakness acted as a strength. Through preemptive diversification away from Pay TV as a main source of revenue, the company claims to have “reached the point of economic indifference” with its Pay TV business model. Calling attention to DTC vulnerabilities demonstrated that programmers have more to lose in this evolving landscape, and the proof is in the bottom line. Disney could have lost $4 billion in yearly free cash flow (FCF) without the new agreement, according to Oppenheimer estimates.

A pivotal aspect of the Charter-Disney deal was its DTC wholesale distribution agreement. Disney+ (the ad-supported tier) and ESPN+ will be provided to an estimated 9-10 million premium Spectrum cable subscribers, sold to Charter on a discounted wholesale basis.

Over the next year, Pay TV providers will follow a similar framework when executing distribution deals with other DTC providers that maintain linear assets. With that said, this will not restore Pay TV to its peak-profit glory days—we anticipate cord-cutting will accelerate in 2024 (see Figure 2 below).

Figure 2: AlixPartners Proprietary Cord-Cutting Model, U.S. Households (MM)

Global TV market growth will begin to level off as Pay TV revenues continue to shrink and the streaming market continues to mature.

As a result of a tapering CAGR, it is unlikely the market will support the 80+ streaming players that exist today globally, leading to streaming consolidation in 2024. In the U.S., we foresee streaming as a “winner-take-most” market with 4-5 winners.

Figure 3: Global TV Market as percentage of world GDP by year1

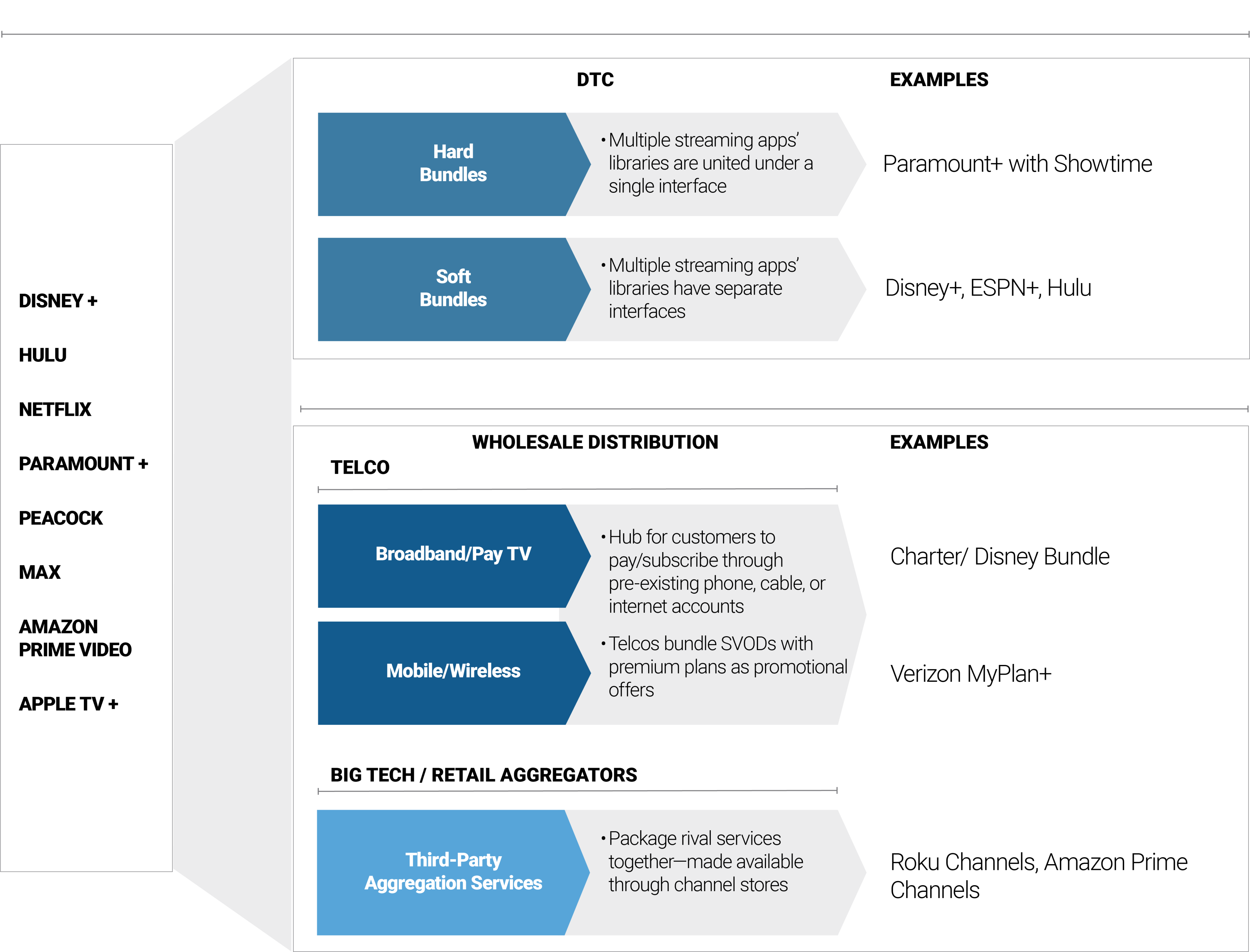

The tides will turn back in favor of bundled offerings.

DTC providers will need to tap into wholesale licensing and distribution to unlock incremental value in streaming markets. According to Omdia, bundles that include Pay TV, broadband, or wireless plans alongside a streaming subscription will generate 70% of OTT video net sub adds.

At the same time, consumers are increasingly overwhelmed by the proliferation of platforms, rising prices, and disparate billing sources for multiple subscriptions. Demand for bundles is growing as consumers crave a simplified experience—more content with fewer apps to flip between—and better value, as they save 20-50% with bundled services vs. subscribing à la carte.

Global estimates forecast that bundles will constitute one-fourth of global subscriptions by 2028. We believe the opportunity for streaming bundles in the U.S. could be even higher than global estimates—with the potential to surpass 50% of total subscription video on demand (SVOD) purchases through telco or aggregator bundles.

The current streaming bundle value chain is a complex ecosystem with more than 1,200 documented partnerships between streaming services and wholesale distributors such as telcos and cable providers.

Figure 3: Global TV Market as percentage of world GDP by year1

We see three key signs that the global TV market is approaching a critical inflection point:

1. Diminishing revenue pool within

Combined with Pay TV subscription and ad revenues will fall to 0.16% World GDP in 2024 (Falling at a negative 3% CAGR since 2017

2. Deceleration in streaming growth

OTT revenues will reach 0.21% World GDP in 2024. However, high double-digit growth of 22% CAGR since 2017 will slow to a 5% CAGR from 2024 to 2026--demonstrating platform maturity (falling at a negative 3 % CAGR since 2017).

3. Approaching maximum consumers are willing to spend on a premium

With rising premium subscription prices, consumers have started seeking alternative OTT offerings.

The tides will turn back in favor of bundled offerings.

DTC providers will need to tap into wholesale licensing and distribution to unlock incremental value in streaming markets. According to Omdia, bundles that include Pay TV, broadband, or wireless plans alongside a streaming subscription will generate 70% of OTT video net sub adds.

At the same time, consumers are increasingly overwhelmed by the proliferation of platforms, rising prices, and disparate billing sources for multiple subscriptions. Demand for bundles is growing as consumers crave a simplified experience—more content with fewer apps to flip between—and better value, as they save 20-50% with bundled services vs. subscribing à la carte.

Global estimates forecast that bundles will constitute one-fourth of global subscriptions by 2028. We believe the opportunity for streaming bundles in the U.S. could be even higher than global estimates—with the potential to surpass 50% of total subscription video on demand (SVOD) purchases through telco or aggregator bundles.

The current streaming bundle value chain is a complex ecosystem with more than 1,200 documented partnerships between streaming services and wholesale distributors such as telcos and cable providers.

Figure 4: Streaming bundles value chain

The pendulum will swing back toward bundled offerings, but to what extent? Different operator bundles encompass varying levels of “invasiveness” to streaming businesses, and DTC providers will want to weigh the trade-offs. Do the upsides of bundles—greater net new subscribers, lower customer acquisition cost, and reduced churn—outweigh the downsides of lower average revenue per unit (APRU) for DTC and a requirement for providers to share more data?

Is the new “Streaming War” becoming the “Streaming Bundles War”?

It remains to be seen whether telcos, big tech companies, or streaming providers themselves will dominate in a world that leans wholesale. Can traditional multichannel video programming distributors (MVPDs) remain the wholesalers of choice in a world without Pay TV if they pivot to provide bundled streaming offerings with virtual MVPD and SVOD?

Figure 5: Smart operators should think about the bundle’s future in three ways

02/05

Artificial intelligence will transform the operational and competitive landscape...

...significantly impacting the advertising and creator economies—but successful integration hinges on a deliberate approach, data transformation, and change management.

Machine learning (ML) and generative AI have the potential to revolutionize production workflows and the content creation process. But the extent to which they do so will depend on the level of disruption that consumers, writers, talent, and producers have an appetite for.

We do not expect generative AI to entirely replace the creative work done by humans, especially for premium content. Lower-quality or high-churn content—such as social media, email marketing, and basic script writing—will be almost fully automated in the next few years. But human beings will continue to do the heavy lifting at the top end of the spectrum.

Instead, we believe AI should be viewed as a powerful tool that complements the creative process, enhancing productivity and capabilities while a human sits in the driver's seat. It can streamline tasks, offer insights, and assist in aspects of content creation that require a lower degree of creativity, such as summarizing or simple editing. This will enable creators to focus on artistry and innovation.

As a result, we should separate the hype from the near-term promise when exploring what GenAI can do for media and entertainment operations. Below, we lay out specific solutions and practical approaches for implementing the technology.

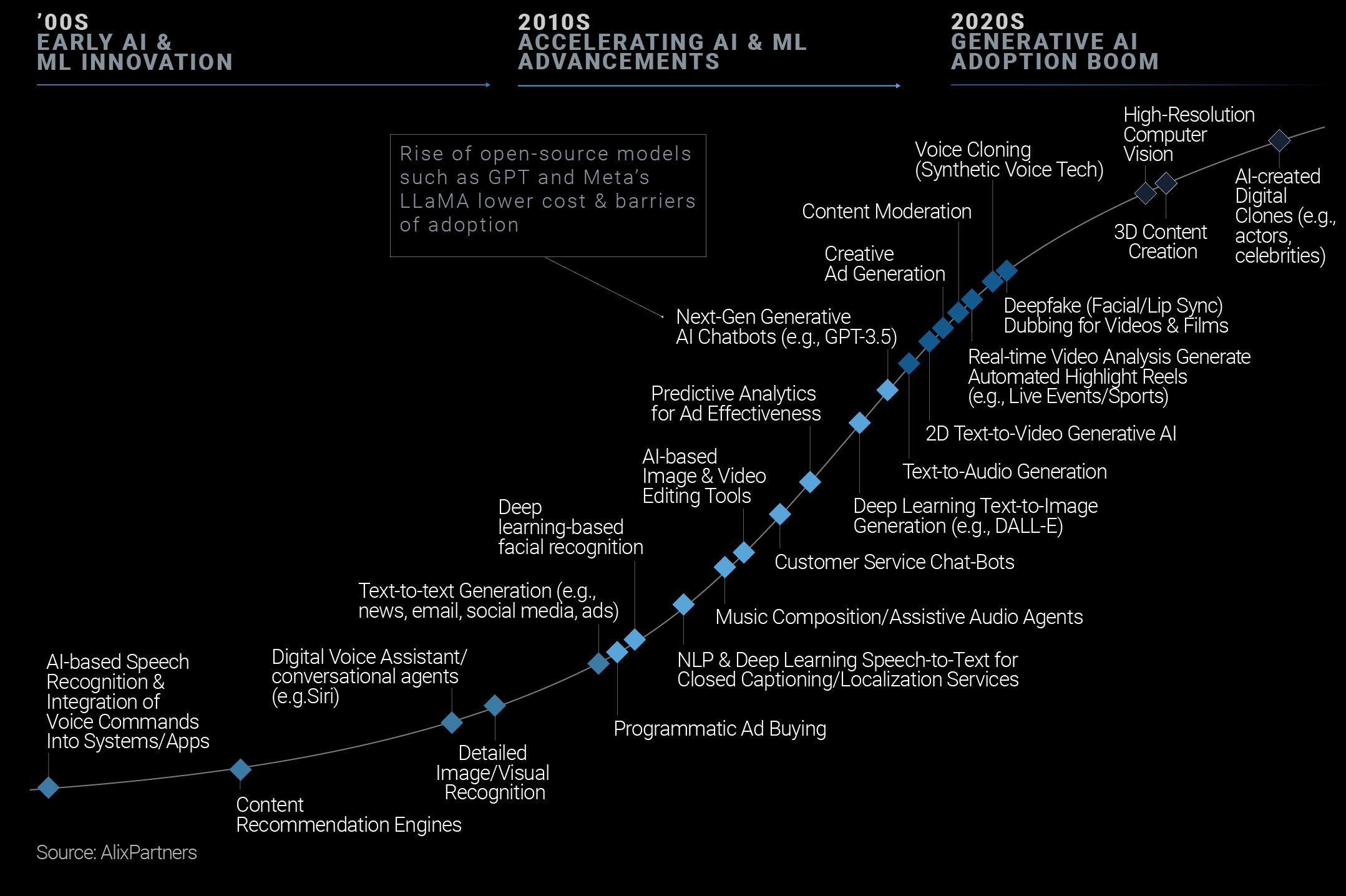

Where is the creator economy on the AI adoption curve?

Figure 6: The creator economy AI adoption curve

Three examples of rising GenAI use cases that we predict will become more widely adopted by the creator economy in 2024:

- Creative ad generation and modification: GenAI-enabled tools can streamline ad creative processes, enhance ad performance, and adapt content effectively—ultimately improving campaign performance and ROI. Third-party vendor tools can automate simple tasks like designing basic visuals and generating text and headlines, and can also apply deep learning to produce personalized ads across various social channels.

- Post-production use cases such as simple editing or deepfake dubbing for localization and transcription services: Companies like Iyuno—used by Netflix during the post-production editing process—are leading the innovation charge in the dubbing and localization services space. Deepfake dubbing leverages AI to generate voiceovers that mimic the lip movements and facial emotions of original on-screen actors. This level of synchronization enhances the overall viewing experience and can make localized content appear more natural and less disjointed. Also, early experimental use cases of voice cloning using AI-enabled synthetic voice technology can generate voiceovers that match original on-screen actors.

As a result of domestic production delays from SAG-AFTRA strikes—the implications of which will extend well into 2024—streaming platforms like Netflix, Apple, and Amazon may increasingly turn to international content to fill gaps in their content libraries for the time being. A shift toward international content could be a near-term accelerator of more widespread deepfake dubbing adoption in film and TV. - Real-time video analysis is boosting monetization for content rights owners: WSC Sports is revolutionizing the sports media landscape by harnessing the power of AI to cut, crop, and distribute automatically generated sports highlight clips in real-time—including transforming horizontal game broadcasts into dynamic vertical video for social and mobile apps. The company, which works with hundreds of leagues and broadcasters, provides its partners with better localization for global distribution and greater personalization through curated highlights by player, type of play, and video duration. This not only streamlines back-end processes but enables faster content delivery which, in turn, enhances fan experience and engagement.

Another example is AI-enabled advanced search for owned IP across audio and video content archives. These tools recognize and label faces, objects, and actions; identify topics, sentiments, and emotions; extract keywords; automatically transcribe speech; and index all captured data for advanced searchability. They also help drive back-end search functions to identify content that can be repurposed across different platforms, maximizing monetization of existing media assets.

Use cases can further extend to user-centric platforms. Tubi, for example, is pioneering a dynamic search feature powered by ChatGPT-4 to assist viewers in navigating its extensive content library of over 200,000 movies and TV episodes. Over time, machine-learning algorithms will yield hyper-personalized recommendations for users, suggesting content that may align with their preferences and moods—giving them less reason to platform hop.

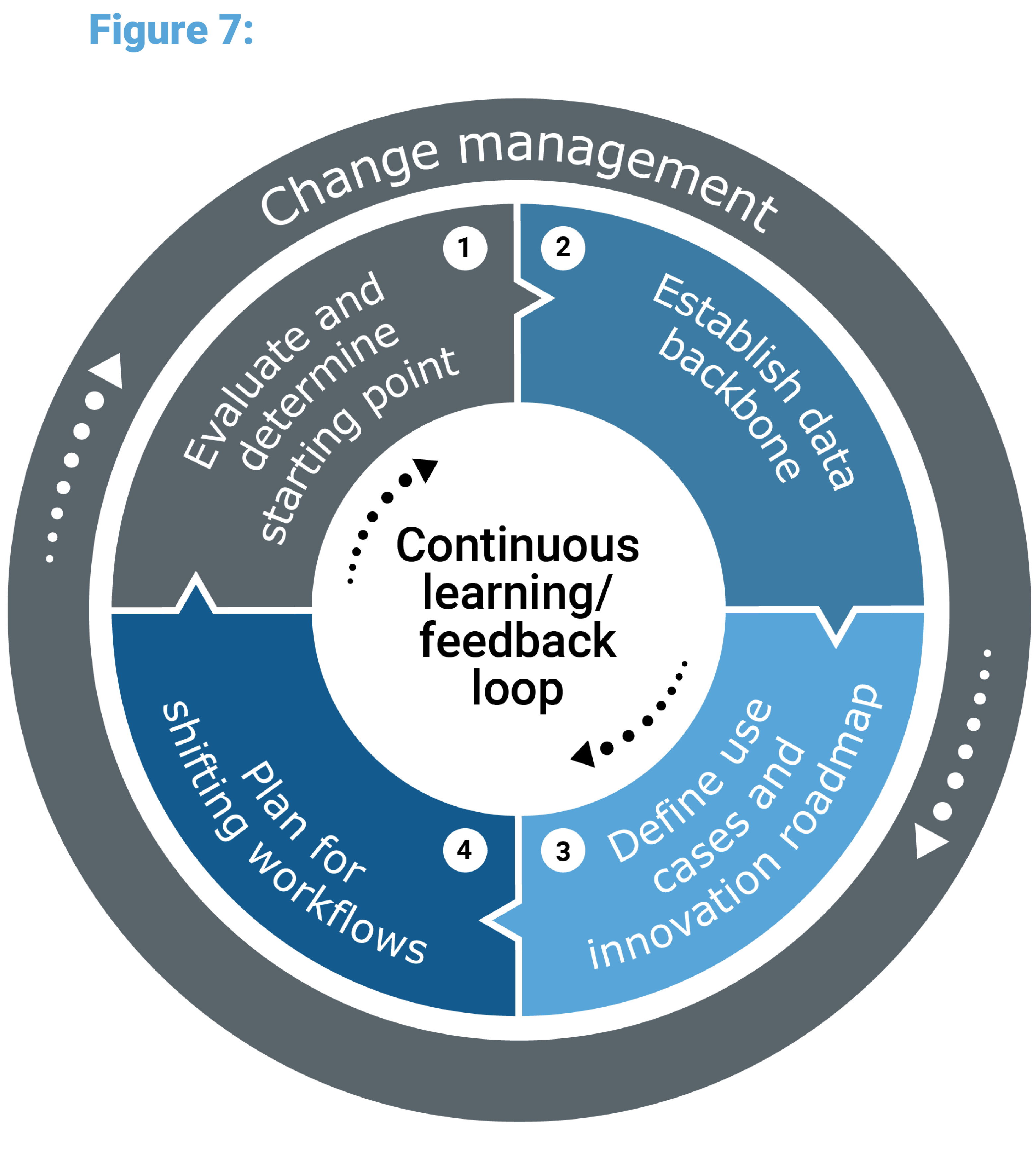

We all are familiar with the story "The Tortoise and the Hare"—and a speed-to-impact approach for AI implementation is similar. Instead of rushing into AI projects with unrealistic speed and ambition, a more prudent approach is to start small and focus efforts where you have ample structured data. Just as the tortoise took measured steps in the race, AI projects should begin with well-defined and manageable use cases. This approach isn't about being slow or passive; rather, it's about being deliberate and methodical.

Approximately 80% of the initial effort in AI and ML projects is dedicated to data wrangling. Media and entertainment companies vary on the maturity scale in terms of mining, structuring, and leveraging data. These companies must assess and determine their starting point based on data readiness. While they have treasure troves of proprietary data, it is often not in good enough shape for ML and GenAI. By addressing issues like granularity, data provenance, duplication, and accuracy, companies can transform their unstructured data into a foundation for scalable ML and GenAI solutions.

Over the next year, media & entertainment companies must cut through the hype and noise and focus on applying a practical approach to create measurable value when integrating AI & ML into operations.

After establishing a structured data backbone, continuous learning through feedback loops is critical. A well-planned and consistent approach to AI implementation increases effectiveness and likelihood of success. It's not about racing to the finish line but about building a sustainable and accurate AI system that can grow over time.

As media businesses pilot new generative AI tools, a challenging next step will be getting humans to do things differently (e.g., accepting and adopting these tools). For example, organizations that utilize AI and ML tools in the marketing function will shift the majority of their staff operations from producing content to more strategic activities like marketing strategy, planning, and market activation (e.g., identifying white space and attacking the market). This transition might also lead to the merging of cross-functional teams. In this evolving landscape, empathy becomes a pivotal factor—caring for the hearts and minds of the people affected will be crucial for operational orientation and effective change management.

Companies should also strike a careful balance between focusing on AI initiatives and pre-existing revenue drivers in the coming year as they navigate how to make AI a profitable venture.

03/05

Moderate ad market recovery and mid-single-digit growth likely in 2024.

In March, we wrote about the evolving challenges affecting the advertising market, shedding light on ad spend headwinds during economic downturns. Our research indicated that the advertising market often faces a prolonged recovery period, spanning an estimated 8 to 19 quarters after the broader economy.

Thus far, the recovery has been volatile. According to Standard Media Index, the U.S. ad market experienced an average monthly decline of -3.8% in the first half of 2023. However, Q3 saw a noteworthy turning point with 6.2% year-over-year growth in July, followed by 1.2% year-over-year growth in August—the first consecutive months of growth since early 2022.

While there are promising signs for the ad market in 2024—the presidential election will provide a $10+ billion boost in the U.S.—it's unlikely digital growth will return to high-double-digit rates seen pre-pandemic. Our prediction for a FY 2024 recovery is in line with industry forecasts, indicating a moderate rebound and mid-single-digit growth for overall ad spend. However, this hinges on broader economic conditions, which remain unclear.

Inflation is a significant factor in this uncertainty. According to AlixPartners’ 2023 U.S. Retail Holiday-Outlook Survey, 44% of consumers think the economy is doing worse now than a year ago, and 34% think the economy will be worse in a year.

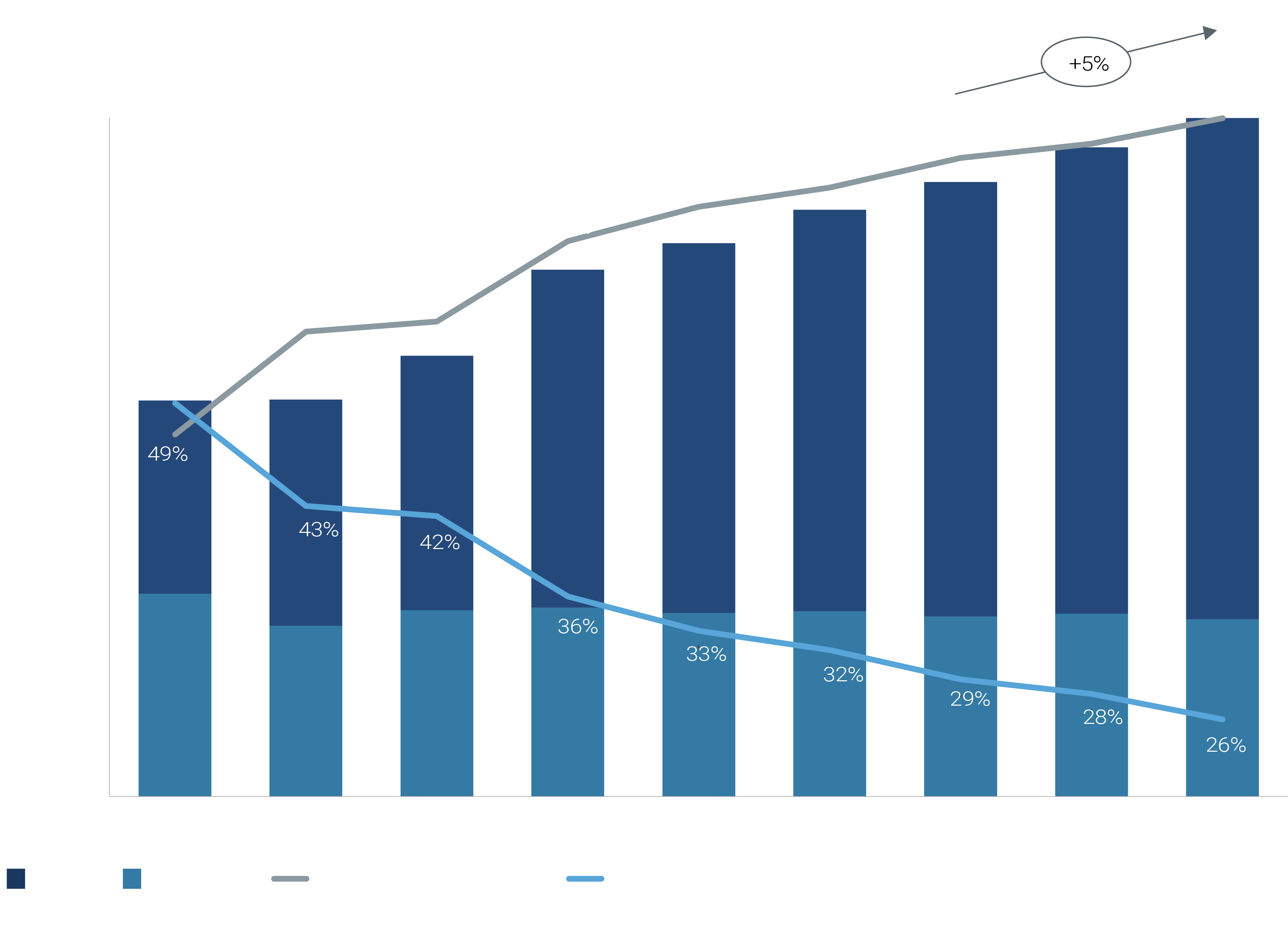

Over the next three years, the global ad market is expected to stabilize at a 5% CAGR, but budget shifts across the advertising value chain are poised to create an uneven recovery across channels and platforms.

Figure 8: Global advertising expenditure by year ($B, USD)

Traditional channel spend will not fully recover to pre-pandemic levels as advertisers will further reallocate budgets to digital platforms.

A recent media agency survey by Digiday found that 49% of advertisers expect budgets to increase in 2024; 43% expect budgets to remain the same and only 8% expect budgets to decrease. But advertisers will allocate budget increases toward digital channels—such as social media, search marketing, digital displays, streaming video, connected TV (CTV), and retail media.

We expect reallocation of traditional channel ad spend from linear TV, print, and radio to total roughly $10-20 billion in 2024. This is in line with a 1-2% global spending reallocation to digital in 2022 and 2023 but demonstrates a leveling off compared to previous years, which saw reallocation rates of 5-7% over the total market.

In times of economic uncertainty, digital advertising platforms provide a valuable benefit. They allow advertisers to swiftly move funds across various platforms like CTV, retail media networks, search, and social media. This flexibility enhances advertisers' ability to adapt to changing circumstances.

CTV is rapidly approaching Pay TV. CTV is on an upward trajectory, on track to capture 39% of total TV ad spend by 2026—posing an imminent threat to Pay TV's dominance over TV advertising. Over the next year, we anticipate market dynamics will accelerate the flow of ad dollars to CTV, potentially hastening a point of inflection.

- Pay TV has been a trusted and reliable platform for advertisers for decades, but its weakening stronghold hinges on tentpole programming like elections, live news, and sports—which will continue to shift toward live-streaming models (more on this later).

- More SVOD price hikes will come in 2024 as providers attempt to draw more subscribers to ad-supported tiers. We anticipate Disney and Netflix advertising video on demand (AVOD) tiers will steadily gain more traction with advertisers this year, but at a slower rate than Amazon. Given the strength of its well-established ad network, demand for ads on Prime Video will be significantly higher than that of other players.

We expect to see divergence in ad revenue growth across social media platforms. Intensifying competition and user growth saturation—approaching 230 million users in the U.S. (67% of the population) with less than 2% user CAGR through 2025—will drive uneven performance for players over the next year. For instance, legacy platforms like Facebook and X (formerly Twitter) will face challenges in retaining users according to forecasts, suppressing advertiser ROI.

Second-tier platforms, such as Snapchat and Pinterest, will find it increasingly difficult to compete with larger rivals even if they serve a niche or offer a differentiated experience in a specific category, such as shopping or online communities.

Fragmentation and saturation are driving large players, namely Meta and TikTok, to expand into new functional areas to retain user engagement, which will create greater convergence.

Platforms moving to innovate with new GenAI tools and advertising services could win greater share. To do so, they must offer a compelling value proposition to attract and retain users and creators, while providing differentiated ad solutions for brands and creators.

2024 will be a pivotal year for advertisers to evolve data & technology strategies to mitigate unforeseen costs and ROI damages.

Amid the evolving landscape for global data privacy regulations, marketers face a growing checklist to comply with the proliferation of policies. Four more U.S. state laws will take effect in 2024, along with talks of federal law for AI and data privacy and tighter EU general data protection regulation (GDPR) enforcement (including the Digital Markets Act and Digital Services Act).

Companies will need to be particularly diligent in maintaining robust data standards and governance practices as the role of AI in marketing and advertising evolves. This will expose new blind spot risks for marketers—who are already required to disclose how they use personal data to power AI tools under GDPR.

As the ad market rebounds, we expect to see scrutiny over digital-dollar allocation in budgets. Instead of an "everything but the kitchen sink" approach, advertisers will funnel a larger portion of their budgets into fewer digital channels that drive higher engagement with their target audiences.

We expect to see divergence in ad revenue growth across social media platforms. Intensifying competition and user growth saturation—approaching 230 million users in the U.S. (67% of the population) with less than 2% user CAGR through 2025—will drive uneven performance for players over the next year. For instance, legacy platforms like Facebook and X (formerly Twitter) will face challenges in retaining users according to forecasts, suppressing advertiser ROI.

Second-tier platforms, such as Snapchat and Pinterest, will find it increasingly difficult to compete with larger rivals even if they serve a niche or offer a differentiated experience in a specific category, such as shopping or online communities.

Fragmentation and saturation are driving large players, namely Meta and TikTok, to expand into new functional areas to retain user engagement, which will create greater convergence.

Platforms moving to innovate with new GenAI tools and advertising services could win greater share. To do so, they must offer a compelling value proposition to attract and retain users and creators, while providing differentiated ad solutions for brands and creators.

2024 will be a pivotal year for advertisers to evolve data & technology strategies to mitigate unforeseen costs and ROI damages.

Amid the evolving landscape for global data privacy regulations, marketers face a growing checklist to comply with the proliferation of policies. Four more U.S. state laws will take effect in 2024, along with talks of federal law for AI and data privacy and tighter EU general data protection regulation (GDPR) enforcement (including the Digital Markets Act and Digital Services Act).

Companies will need to be particularly diligent in maintaining robust data standards and governance practices as the role of AI in marketing and advertising evolves. This will expose new blind spot risks for marketers—who are already required to disclose how they use personal data to power AI tools under GDPR.

04/05

Regulatory scrutiny and a high cost of capital will likely limit a rebound in media consolidation...

...but legacy media carve-out activity will drive dealmaking in 2024.

As we examine the menu for media industry dealmaking in the upcoming year, it's evident that there are both sweet and sour ingredients. The Federal Reserve's expectation to maintain interest rates above 5% until 2024 will be a significant headwind. A higher-for-longer rate environment will intensify the difficulties faced by those seeking to secure debt financing for mergers and acquisitions, further complicating the dealmaking landscape.

We also anticipate greater regulatory actions aimed at curbing antitrust and anticompetitive practices will result in blocked tech and digital media acquisitions in 2024.

Due to these factors, it's unlikely that we will see a substantial surge in media deal volume in 2024 beyond a slight uptick. But we see some areas across the ecosystem where dealmaking activity could gain momentum.

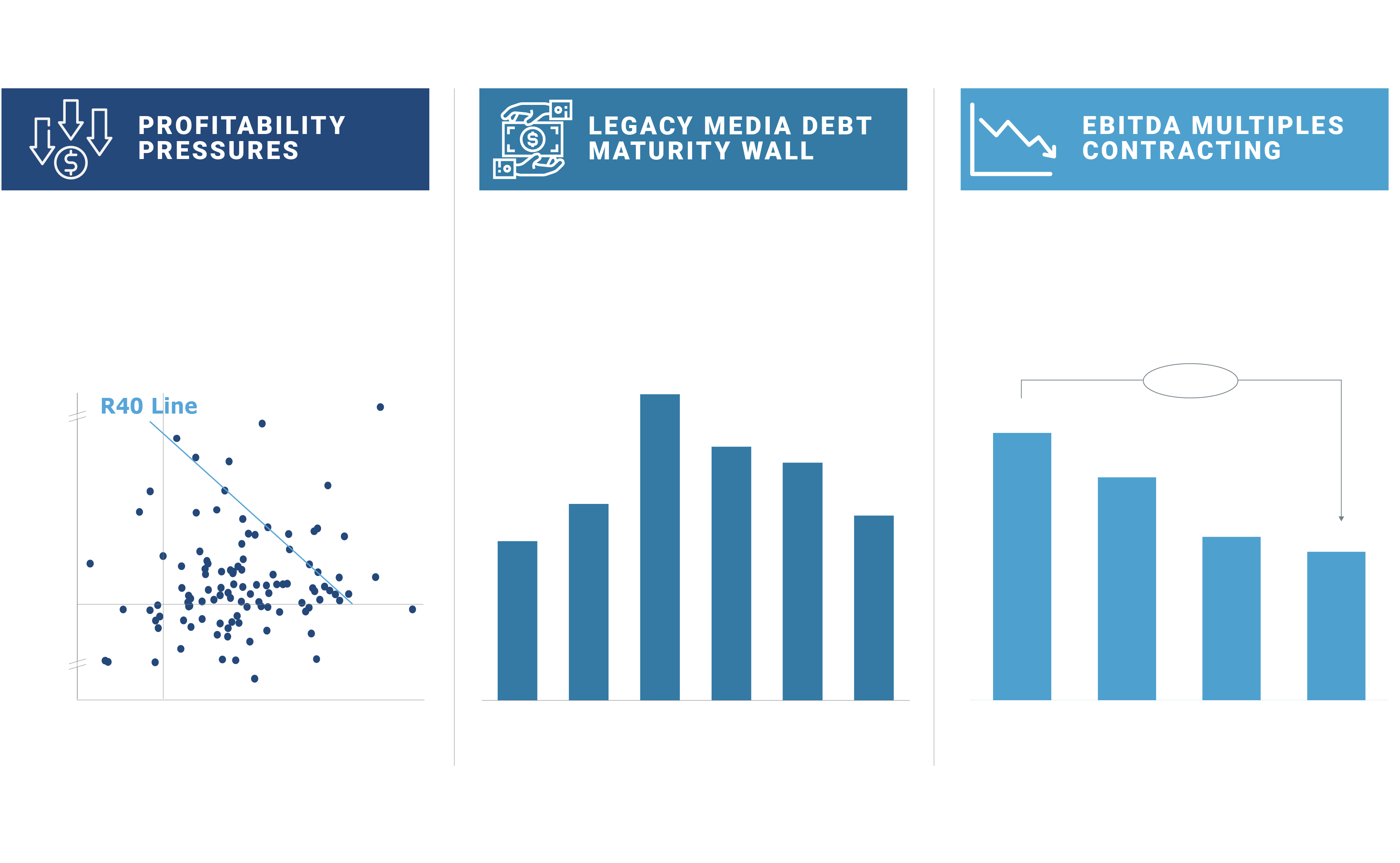

Figure 9: We see three factors driving the opportunity for legacy media consolidation and carve-out activity

Legacy media assets retain significant underlying IP value, and operational transformation can drive value creation and unlock profit opportunities.

Heightened regulatory scrutiny can pose substantial obstacles for industry peers and direct competitors looking to acquire these assets. Under certain circumstances where parent companies face pressure to divest noncore assets for cash, private equity deals may emerge as a more attractive and mutually beneficial option.

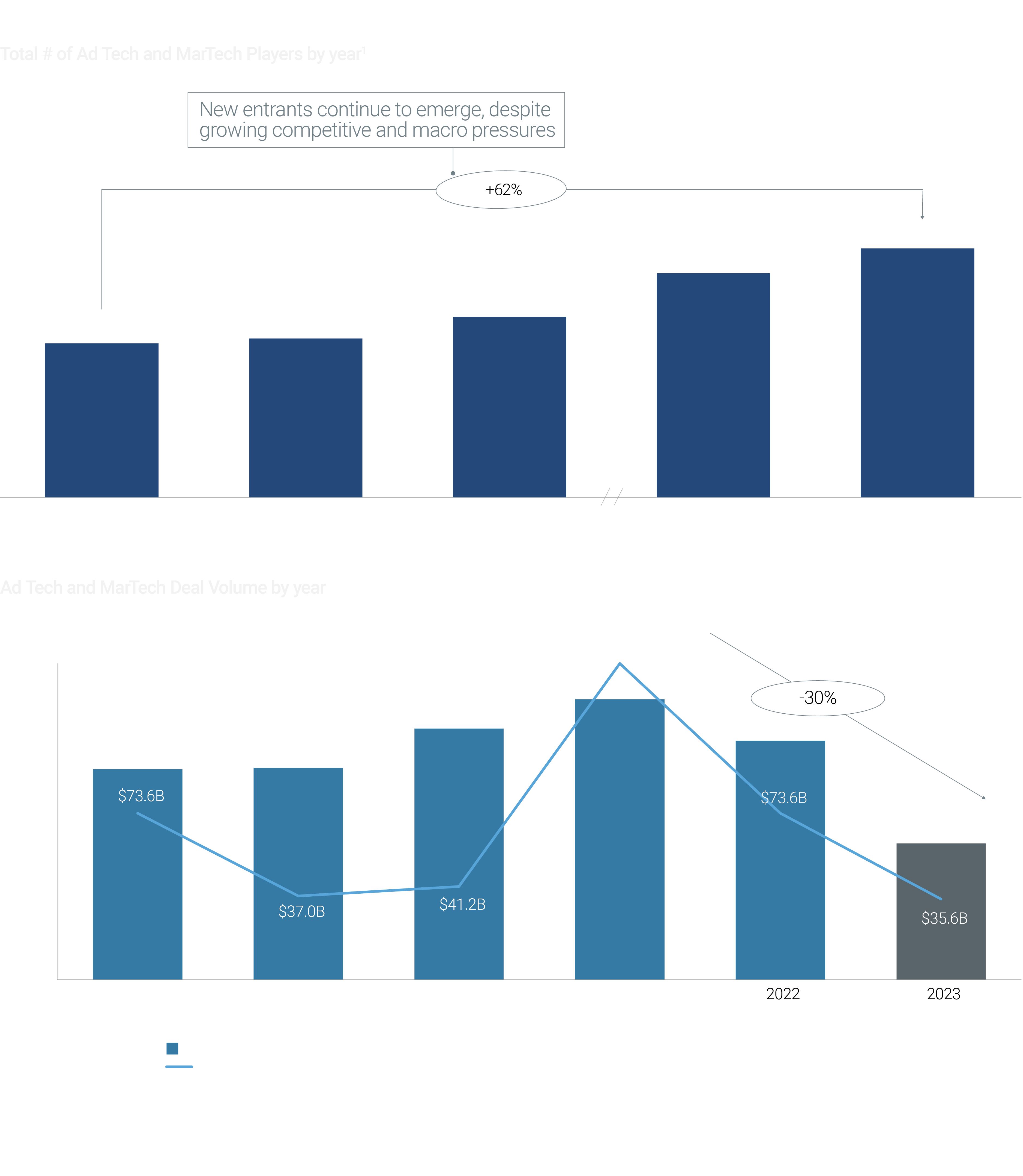

More ad tech consolidation to come, but first more partnerships.

Dealmaking in the ad tech space blossomed in 2021, only to be disrupted by worsening economic conditions before reaching a point of inflection (see below). Consolidation will likely reaccelerate in the coming years as the number of players continues to grow (see below), but the high cost of capital could delay any significant influx of dealmaking in the space.

Instead, we expect more strategic partnerships and collaboration among ad tech vendors in 2024.

Worsening ad market saturation has made it challenging for vendors to generate strong cash flows. Also, marketers across industries will keep looking to consolidate their ad and MarTech stacks to lower costs and improve supply path optimization (SPO), emphasizing the need for a strong value proposition to become a preferred vendor.

Greater demand for a single or unified ad server will drive the proliferation of creative collaborations along the ad tech value chain. Enhanced access to a broader customer base sourced through synergistic partnerships, along with new revenue, will help drive continued value creation. This shift towards collaboration marks a new way of doing business in ad tech, providing new solutions to sustain a competitive edge and secure a prominent place in the market. Companies will need to be more discerning in choosing the right partnerships to go to market, with an eye toward emerging spaces like CTV and retail media. We believe successful partnerships will be a strong foundation for future M&A pairings when dealmaking conditions improve.

Figure 10: Ad Tech & MarTech landscape

05/05

2024 will be a year of reinvention and reinvestment in the future of local news.

Local news has been in decline since the start of the digital boom. Its traditional economic model, heavily reliant on advertising for revenue, has been disrupted by tectonic shifts in the media and technology landscape. As social media, big tech, and digital video platforms captured the lion’s share of media consumption, advertisers followed—leaving little market share for traditional local news.

The growing pressure on the industry has triggered consolidation, leading to less diversity, variety, robustness, and community-centric news. As local news fades in pockets across the U.S., entire communities are left without essential coverage. These headwinds have also triggered a nascent period of reinvention in local news, in which the traditional business model can evolve with new ideas and approaches.

This year will be a period of transformation and renewal for local broadcast news, as networks focus on high-quality, relevant, and engaging programming.

A market correction for peak TV content will extend to local TV broadcasting, and network affiliates will look to streamline operations and balance content volume with quality and relevance. A greater focus on hyperlocal and personalized content will be a differentiator that fosters a strong connection with local communities. Cox has introduced "Neighborhood TV," an innovative streaming news service that delivers hyperlocal, niche content to small zones around a six-to-eight-mile radius in Georgia and North Carolina.

Expanding reach through digital channels will accelerate as more linear TV channels become available on free ad-supported TV (FAST) and live-streaming models. Embracing a multiplatform distribution model is table stakes for retaining traditional broadcast audiences and reaching fragmented audiences. For example, local broadcasters tapping into traditional over-the-air, as well as CTV, mobile, and internet platforms, can claim a larger share of political ad spend during the 2024 elections.

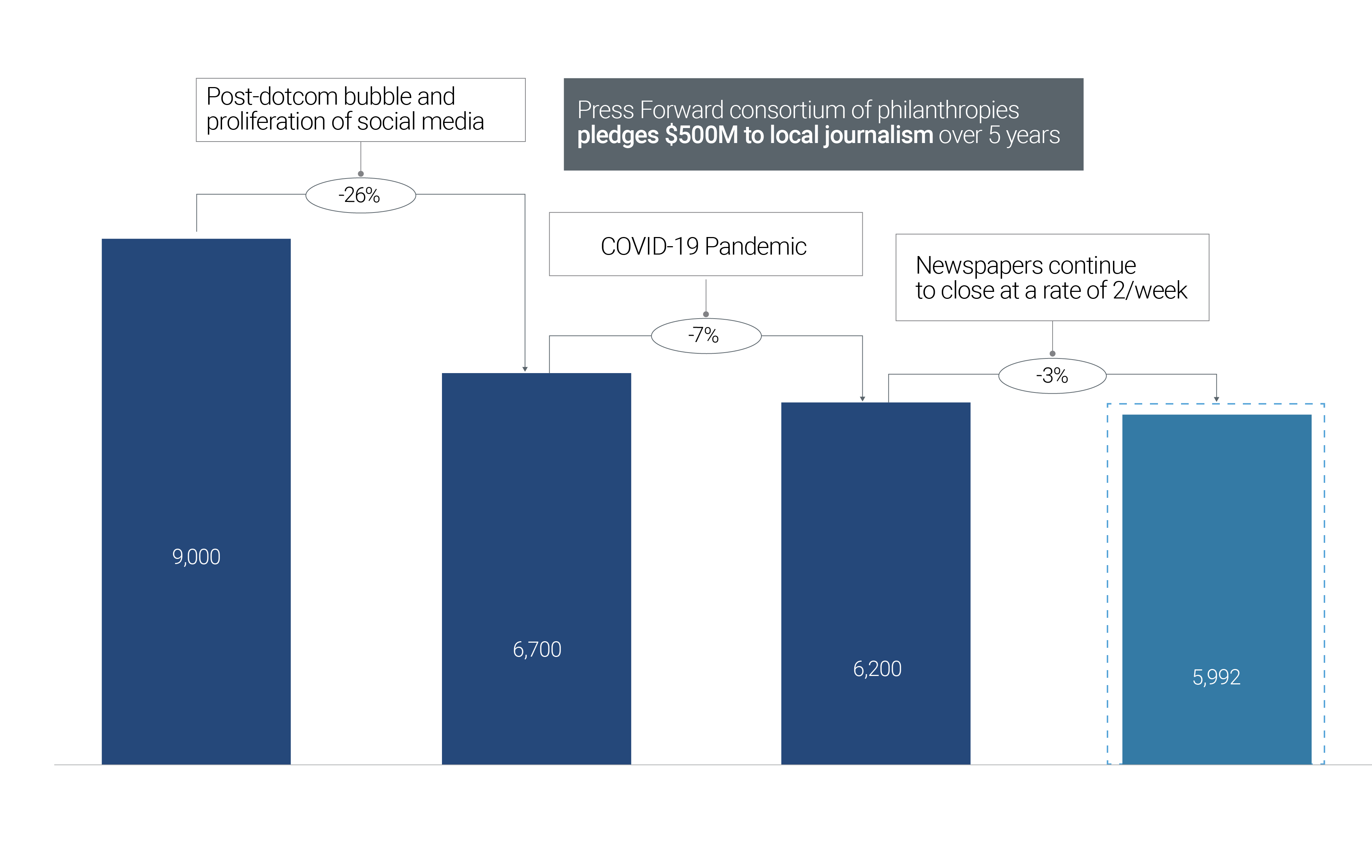

Figure 11: Newspapers have been in continuous decline since the dotcom era, but a new philanthropic approach could mitigate or reverse future declines

However, a commitment to multiple platforms can dilute local news products and contribute to journalist burnout. According to E.W. Scripps (“Scripps”) CEO Adam Symson, supporting a multiplatform approach requires a shift from traditional operations and processes and a renewed commitment to quality journalism. During the first half of 2023, Scripps leadership aligned on an ambitious four-point plan to reinvent and reinvest in local news:

- Emphasize beat reporting and community-relevant issues.

- Leverage technology to reallocate resources to journalism.

- Invest in the future of journalism by investing in its people.

- Integrate Scripps News coverage more deeply into its local news products.

As a core part of its objective to provide fact-based news coverage with deeper context, Scripps will add 250 resources to local reporting teams and invest $10 million to increase journalist compensation. The fuel to reinvest in these areas was largely funded through tech modernization, allowing Scripps to shift production resources towards more reporters and news-gathering staff.

Local newspapers and publishers face a gloomier outlook. However, business model innovation and a push to revitalize local journalism will help offset declines.

The problem could get worse before it gets better as large owners of local newspaper subsidiaries warn about a further reduction to the number of outlets aimed at serving local communities. While shared resources and economies of scale result in cost savings, local news outlets struggle with significantly lower digital subscription revenues vs. print. Intense competition from various free alternatives and social media further erodes revenue, forcing for-profit news organizations to pivot to survive.

Although the future of local journalism may appear bleak, there is room for optimism, especially with the emergence of new philanthropic models. We anticipate more news organizations will transition from private businesses to nonprofit models such as cooperatives or community-based organizations.

In some cases, new outlets are emerging to replace local papers that have shut down. In Marblehead, MA, the legacy local paper dropped local coverage in favor of wire service content, but three new outlets emerged with varying go-to-market approaches. One of the two print-and-digital news sources is a non-profit collective. A third is a digital-only volunteer-run organization. This diversity in approach indicates an environment rich with experimentation to find sustainable solutions.

Figure 12: Publishers should think about new approaches to drive long-term sustainability

Perspectives on Local News Trends

Scripps | Interview with COO Lisa Knutson

In an interview with AlixPartners Partner & Managing Director Jeff Goldstein, Scripps Chief Operating Officer Lisa Knutson shares her views on local tv trends, the overall Scripps transformation, and the strategic benefits it has driven for the organization.

Scripps | Interview with SVP of Local News Sean McLaughlin

In an interview with AlixPartners Director Ade Obatoyinbo, Scripps Senior Vice President of Local News Sean McLaughlin discusses the innovations, efficiencies, automation, and re-investments in their local news organization.

CONCLUSION

Change is the only constant—but the media ecosystem remains ripe with opportunity for innovative players to win and grow

At AlixPartners, we have deep experience working with management teams and investors to help media companies stay ahead of market shifts. By evaluating key operational and strategic levers across the business, we help media companies drive value creation and profitable growth.

As we enter 2024, we believe our five core predictions will determine the future direction of the industry:

- Wholesale distribution will fuel subscriber growth for streaming services—bringing operators and streamers together as companies search for a long-term replacement for the Pay TV model.

- Artificial intelligence will transform the operational and competitive landscape, but successful integration hinges on a deliberate approach, data transformation, and change management—although we do not expect generative AI to replace human creative output, especially around premium content.

- Moderate ad market recovery and mid-single-digit growth is likely—but this hinges on macroeconomic conditions that remain unclear.

- Regulatory scrutiny and a high cost of capital will limit a rebound in M&A activity—but legacy media carve-out activity will drive dealmaking.

- 2024 will be a year of reinvention and reinvestment in local news—in which the traditional business model can evolve with new ideas and approaches.

Meet the authors

By selecting any external link on www.AlixPartners.com, you will leave the AlixPartners website and jump to an unaffiliated third-party website. AlixPartners is not response for the content on any such third-party website, and such website may offer a different privacy policy and level of security. The third party is responsible for website content and system availability. AlixPartners does not offer, endorse, recommend or guarantee any content, product or service available on that third party’s website. The opinions expressed are those of the authors and do not necessarily reflect the views of AlixPartners, LLP, its affiliates, or any of its or their respective professionals or clients. This article AlixPartners 2024 Media and Entertainment Industry Predictions Report (“Article”) was prepared by AlixPartners, LLP (“AlixPartners”) for general information and distribution on a strictly confidential and non-reliance basis. No one in possession of this Article may rely on any portion of this Article. This Article may be based, in whole or in part, on projections or forecasts of future events. A forecast, by its nature, is speculative and includes estimates and assumptions which may prove to be wrong. Actual results may, and frequently do, differ from those projected or forecast. The information in this Article reflects conditions and our views as of this date, all of which are subject to change. We undertake no obligation to update or provide any revisions to the Article. This Article is the property of AlixPartners, and neither the Article nor any of its contents may be copied, used, or distributed to any third party without the prior written consent of AlixPartners. ©2023 AlixPartners, LLP