THE CRITICAL

CONSUMER 2024

The major changes in consumer sentiment across EMEA

A lingering post-pandemic crunch, fuelled by inflation and interest rate rises, has cut household budgets in 2023, resulting in heightened brand competition for this constricted discretionary spend. Retail, Consumer Products, Restaurants, Hospitality, Travel, and Leisure industries are among those hit the hardest. They rely heavily on the volume and frequency of discretionary spend, which can fade rapidly during periods of economic uncertainty. This looks set to continue into 2024.

For businesses to maintain share or grow in this climate, they must deeply understand how these changes impact shoppers. How are their purchasing habits evolving – and how do budgetary pressures and economic insecurities fold into these behaviours?

To find the answers, AlixPartners has conducted an in-depth consumer priorities study across the EMEA region. Over 10,000 shoppers from the UK, France, Germany, Italy, Saudi Arabia, Switzerland, and UAE shared their personal purchase intentions and shopping preferences now, and into 2024.

Our report gives in-depth analysis on how consumer sentiment has shifted and where spending habits will turn next across five areas:

1.Spending intentions

Where consumers are spending now and next

2.Category evolution

Purchase intent and trade-off across category

3.Omnichannel targeting

Preferences across online and offline

4.Customer personalisation

Experiences across all touchpoints

5.Use of technology

Interaction and adoption of technology

What did consumers say, and what do you need to know?

The key findings and valuable insights for consumer-facing businesses:

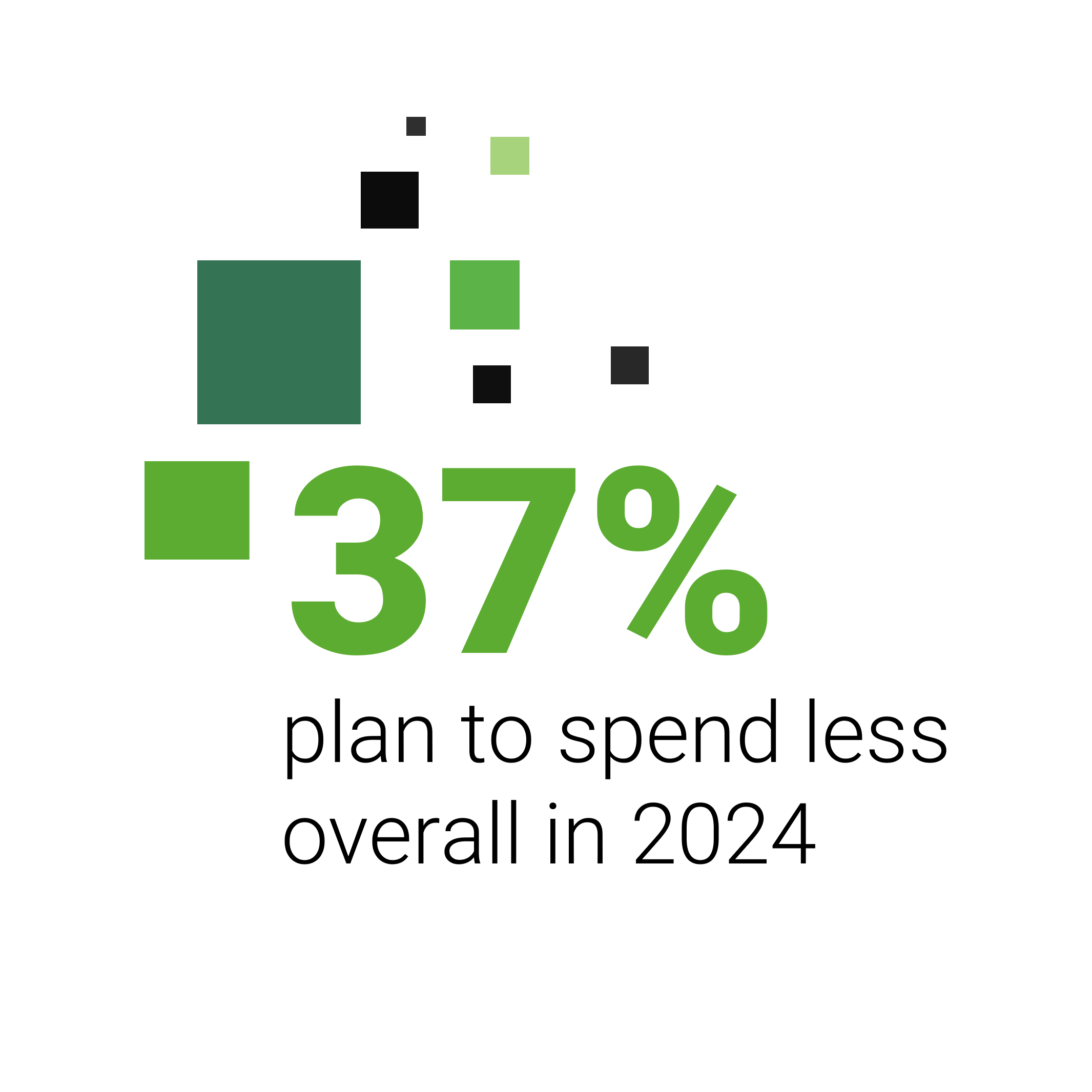

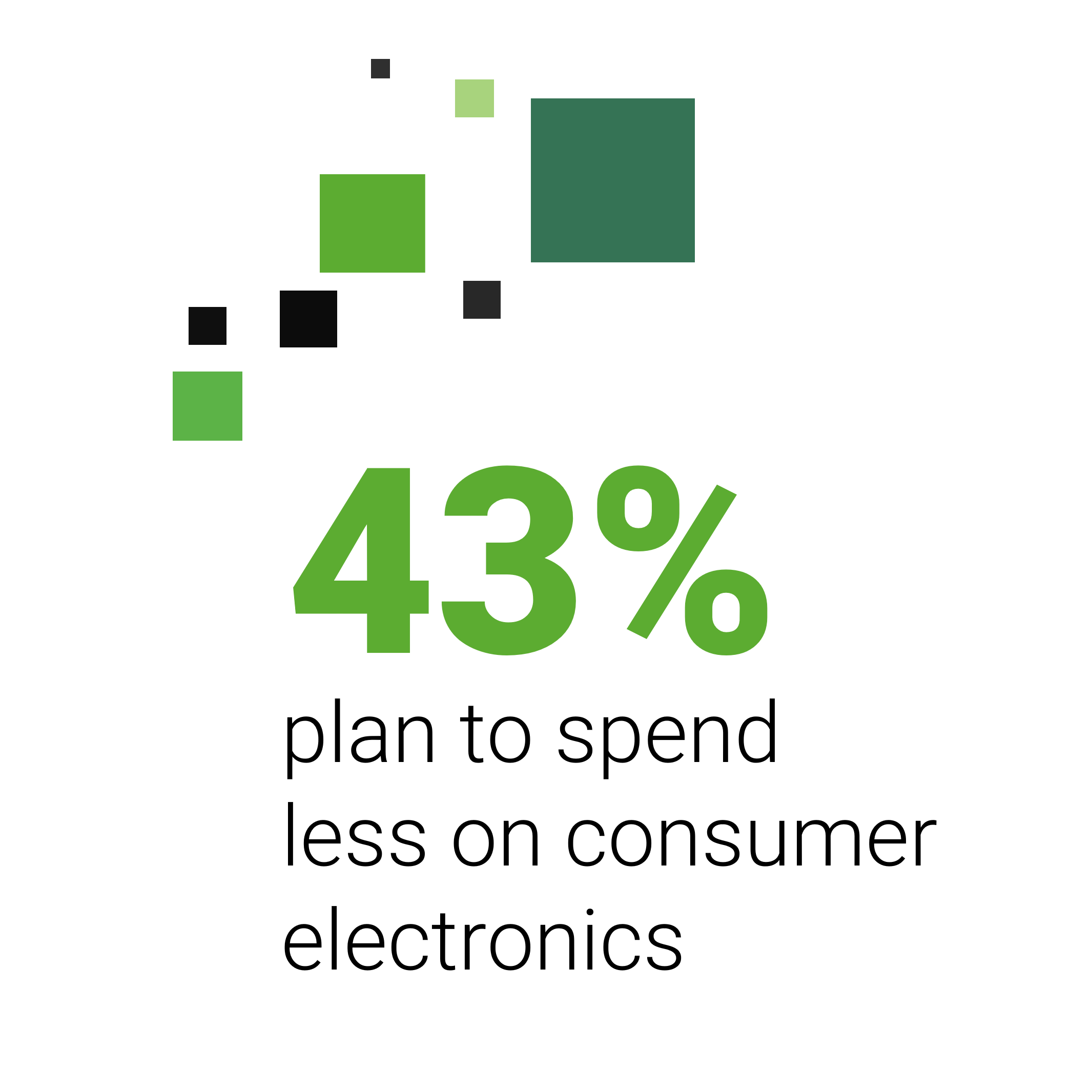

Despite inflation slowing, consumers will spend less in 2024.

Irrespective of income levels, price matters to everyone. In addition, data suggesting that spending levels across income groups will remain the same or increase may still translate to lower buying volumes, given the persistent effects of inflation.

What do you need to know?

Retail, Consumer Products, and Leisure companies must ensure their products are “value-right,” providing strong perceived value for money and quality in categories where shoppers are targeting cutbacks, irrespective of their income levels.

Affordability and curation of range are key due to lower disposable income.

Consumers plan to net spend less across all sectors. This applies particularly to non-food (where purchase decisions will be held back) as well as leisure sectors (where more time will be spent at home and the frequency of visits is expected to reduce).

What do you need to know?

Value for money and perceived value is uppermost in the minds of EMEA consumers. From an e-commerce perspective, consumer product companies must collaborate with retail partners to improve online merchandising and listing positions within category pages, which will boost consumer product awareness, understanding, and consideration.

Channels must be optimised for a customer experience that caters to different types of consumer.

Age plays a significant role in preferred channel communications and omnichannel journey, so must be accounted for through personalised experiences.

What do you need to know?

Productivity improvements are key to elevating the shopping journey across demographics – but be careful not to push out groups less familiar with digital advances. Consider this data when designing marketing and promotional strategies, as well as new concepts at the POS.

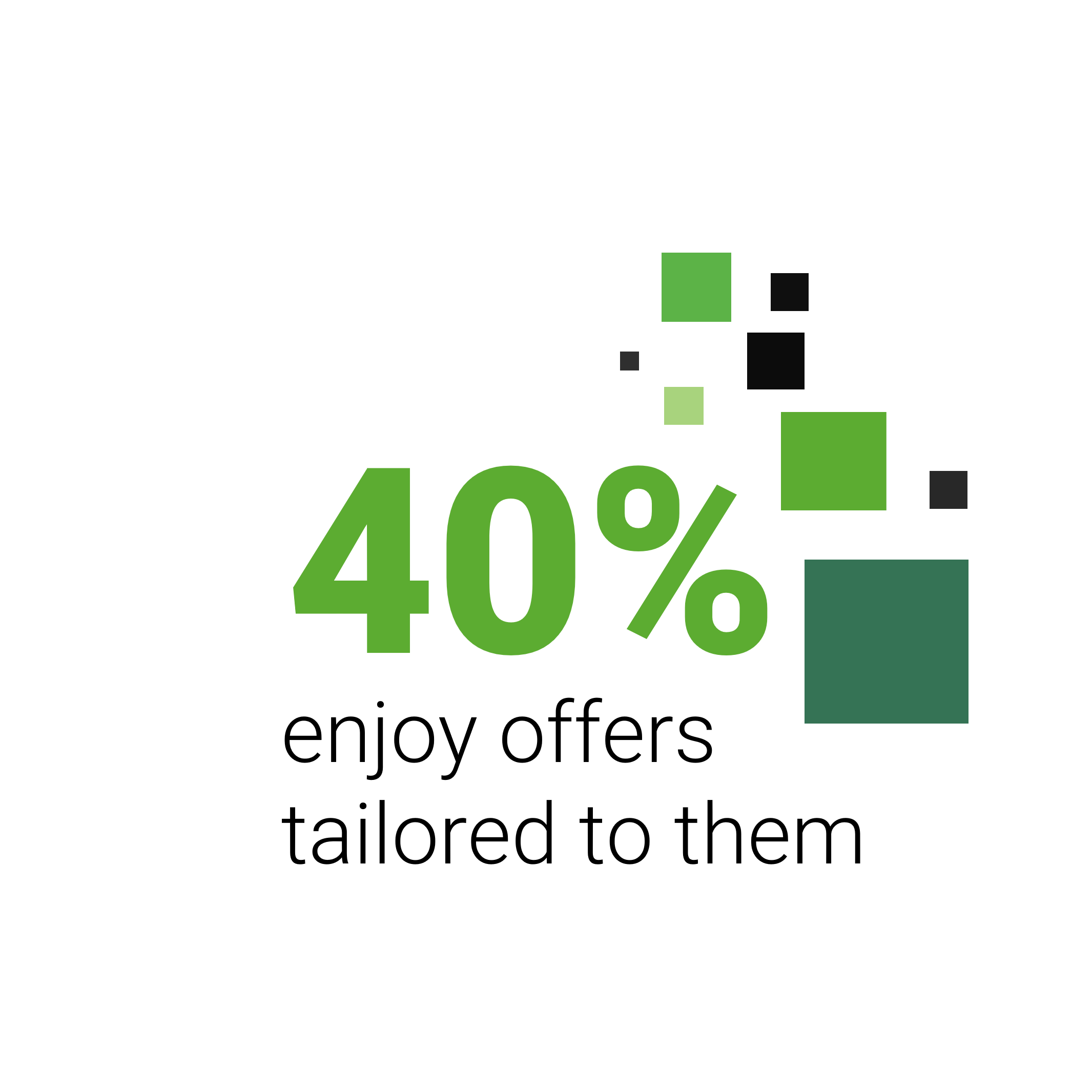

Personalised shopping experiences are essential to improve loyalty and mitigate price wars.

Omnichannel and digital interactions increasingly becoming the standard, consumers enjoy receiving offers tailored to their specific demographics, as opposed to promotions inclusive of all consumers - especially true of high-income and younger consumers.

What do you need to know?

Efforts to enhance customer loyalty must extend beyond pricing. Consumers expect personalisation, and the companies that can

tailor a user experience that resonates with different customer segments across touchpoints will be more attractive and can

gain a competitive advantage.

Strategic technology improves the shopping experience while reducing cost to serve.

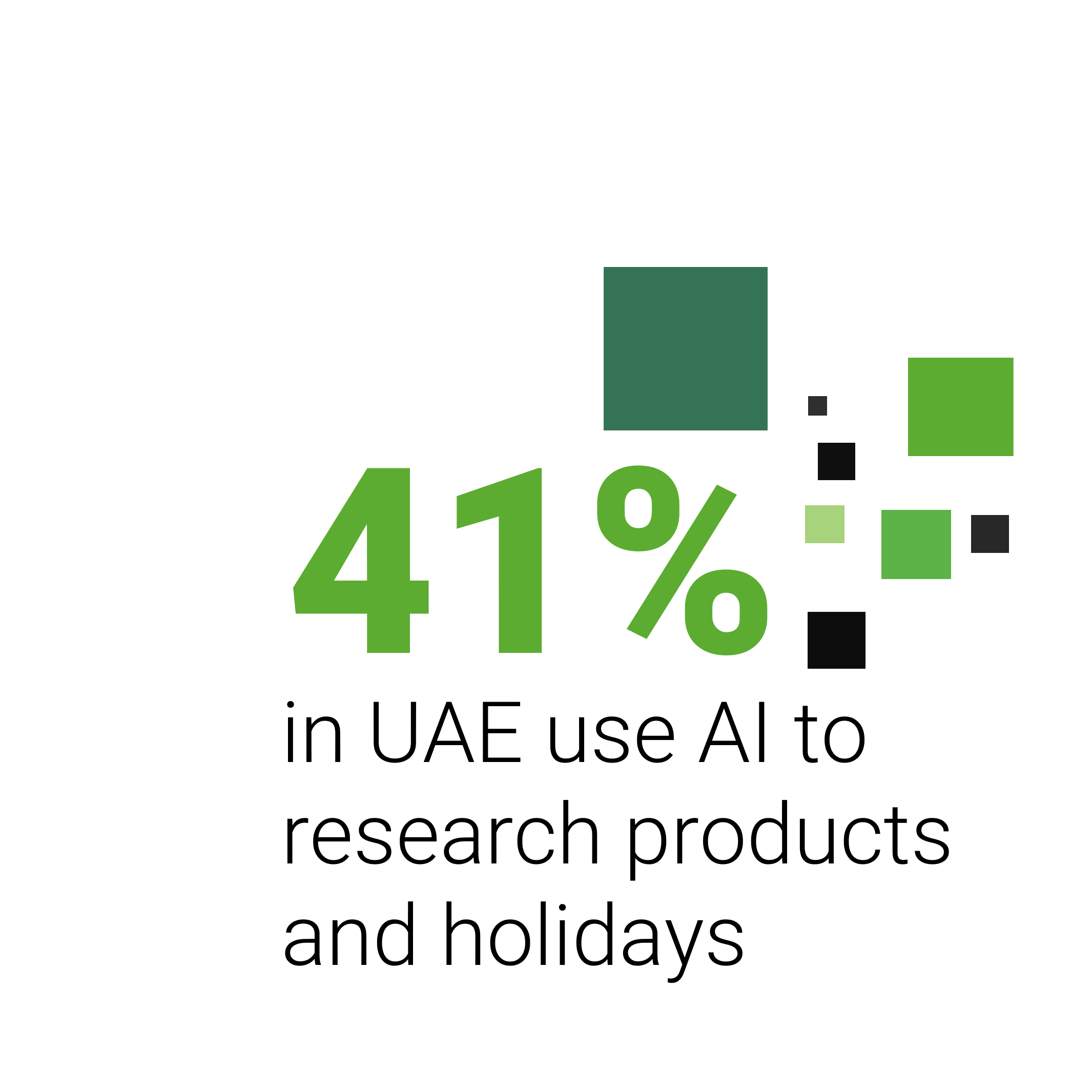

Consumers are willing to explore and adopt other new technologies as they emerge in consumer-facing industries, with more and more using click and collect, digital payments, home delivery services, or retailers’ mobile apps.

What do you need to know?

Consumers show enthusiasm to try the latest digital offerings. This provides a key differentiating opportunity for retailers, given shoppers’ willingness to adopt new technologies and their curiosity and desire to experiment.

Quality is key to success in Restaurants, Travel, Hospitality and Leisure.

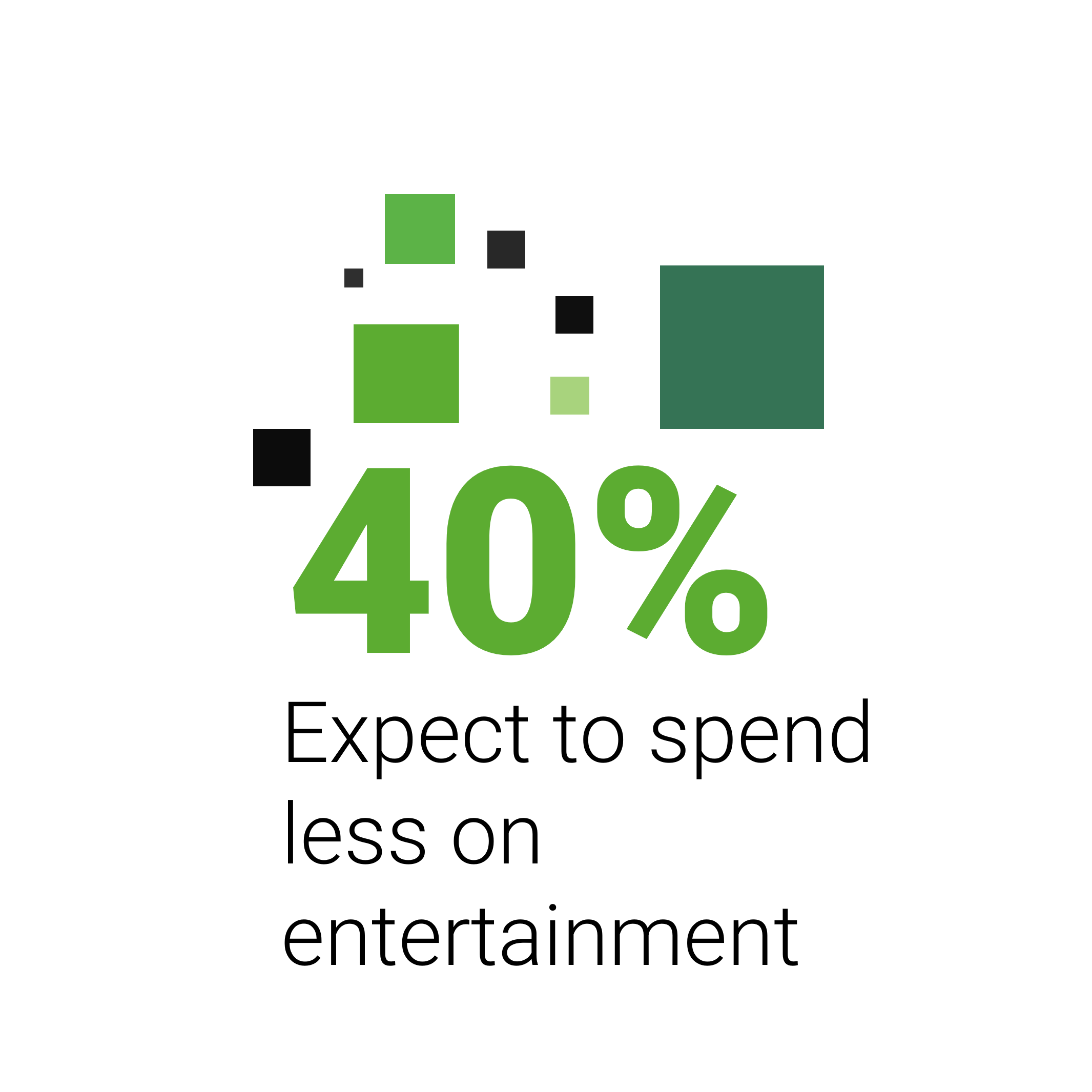

Net spend intentions will dip amongst consumers for discretionary entertainment and leisure activities in 2024.

What do you need to know?

While consumers may reduce spend overall in these sectors, they will be reticent to trade down on quality, instead reducing the frequency of activity to focus on special occasions or fewer, but higher quality, travel, and F&B occasions.

Read the in-depth Critical Consumer 2024 report

For more information, contact us: